Charles Hall is a practicing CPA and Certified Fraud Examiner. For the last thirty-five years, he has primarily audited governments, nonprofits, and small businesses.

He is the author of The Little Book of Local Government Fraud Prevention, The Why and How of Auditing, Audit Risk Assessment Made Easy, and Preparation of Financial Statements & Compilation Engagements. He frequently speaks at continuing education events.

Charles consults with other CPA firms, assisting them with auditing and accounting issues.

The Government Accountability Office just issued the new Yellow Book titled Government Auditing Standards 2018 Revision.

Get Your Free Copy

An electronic version of the 2018 Yellow Book can be accessed on GAO’s Yellow Book web page at http://www.gao.gov/yellowbook.

Major Changes

The introduction to the new Yellow Book summarizes the significant changes as follows:

This revision contains major changes from, and supersedes, the 2011 revision. These changes, summarized below, reinforce the principles of transparency and accountability and strengthen the framework for high quality government audits.

All chapters are presented in a revised format that differentiates requirements and application guidance related to those requirements.

Supplemental guidance from the appendix of the 2011 revision is either removed or incorporated into the individual chapters.

The independence standard is expanded to state that preparing financial statements from a client-provided trial balance or underlying accounting records generally creates significant threats to auditors’ independence, and auditors should document the threats and safeguards applied to eliminate and reduce threats to an acceptable level or decline to perform the service.

The peer review standard is modified to require that audit organizations comply with their respective affiliated organization’s peer review requirements and GAGAS peer review requirements. Additional requirements are provided for audit organizations not affiliated with recognized organizations.

The standards include a definition for waste.

The performance audit standards are updated with specific considerations for when internal control is significant to the audit objectives.

Effective with the implementation dates for the 2018 revision of Government Auditing Standards, GAO is also retiring Government Auditing Standards: Guidance on GAGAS Requirements for Continuing Professional Education (GAO-05-568G, April 2005) and Government Auditing Standards: Guidance for Understanding the New Peer Review Ratings (D06602, January 2014).

Effective Dates

The 2018 revision of Government Auditing Standards is effective for financial audits, attestation engagements, and reviews of financial statements for periods ending on or after June 30, 2020, and for performance audits beginning on or after July 1, 2019.

Early implementation is not permitted.

The 2018 revision of Government Auditing Standards supersedes the 2011 revision (GAO-12-331G, December 2011), the 2005 Government Auditing Standards: Guidance on GAGAS Requirements for Continuing Professional Education (GAO-05-568G, April 2005), and the 2014 Government Auditing Standards: Guidance for Understanding the New Peer Review Ratings (D06602, January 2014).

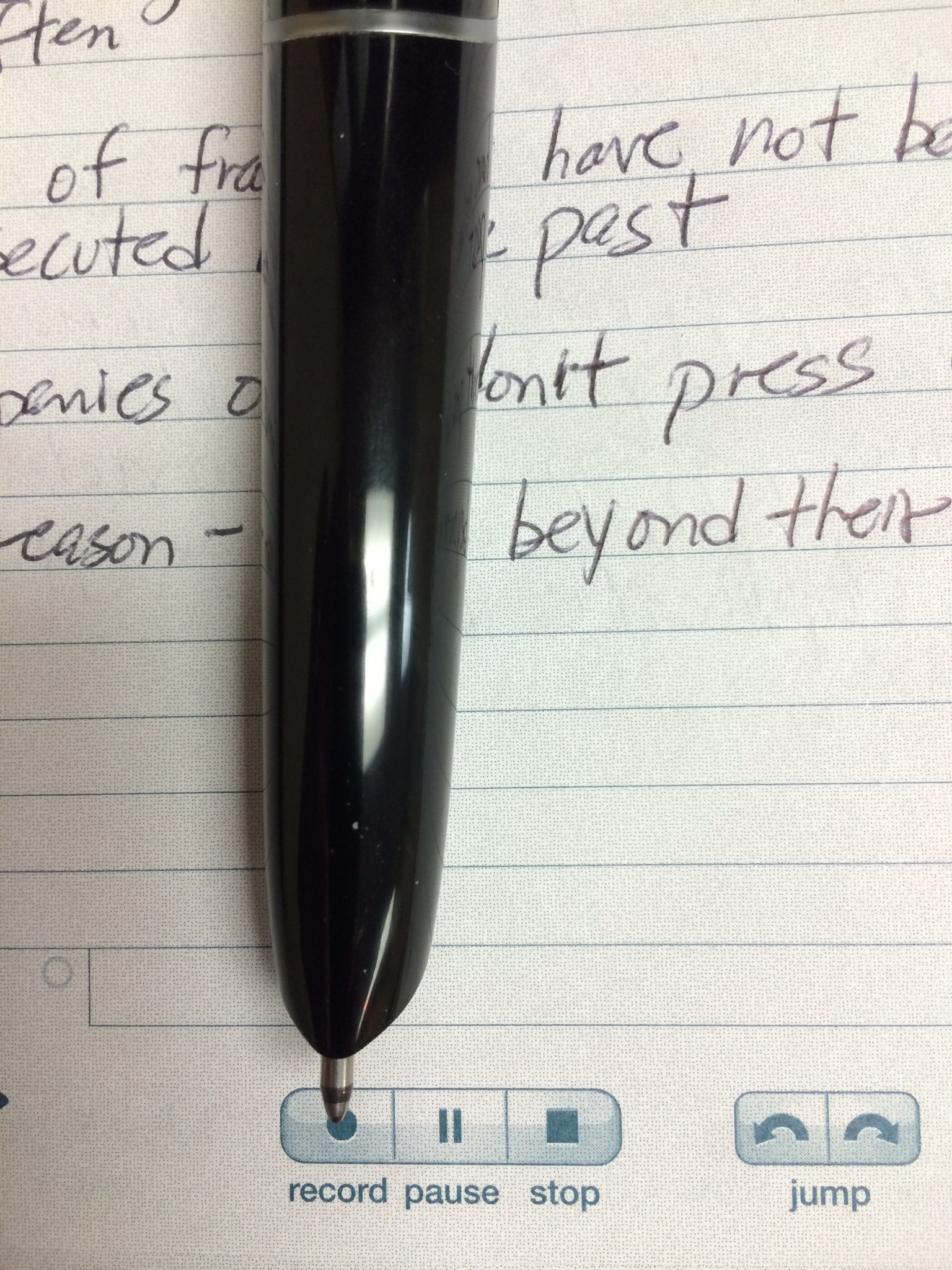

Livescribe: Note taking magic. Here’s an overview of how auditors are making their lives easier using the Livescribe pen.

Have you ever interviewed a client, feverishly taking notes, and straight away forgot critical facts? You wish you had a recording of the conversation. Better yet, you wish you could touch a particular word in your notes and hear the words that were being spoken at that moment. What if I told you, “you can”?

What is Livescribe? It’s an electronic pen/recorder. As you write on special coded paper, you simultaneously record the conversation (the recorder is built into the pen). Once done, you touch a particular letter in a word (with the tip of your pen) and you hear–from the pen–the words spoken at that moment. No more forgetting and not being able to retrieve what was said. And it’s efficient since you can go to any particular part of the conversation using your notes as signposts.

To start a recording, you press the tip of the pen to the “record” icon at the bottom of the page.

To stop the recording you press the “stop” icon above.

Once the recording is complete, you simply touch the tip of the pen to any letter and the audio recording will start playing–from the pen–at that point.

You can upload the pen notes and the audio to your computer desktop Livescribe software using a USB cord that connects to the pen. (See below.)

You can also play back notes from your uploaded desktop copy just as you can with your pen. Click a letter with your mouse and the recording will play.

I was surprised by the clarity of the sound from the pen and the audio capacity–200 hours (for the Echo version that you see below).

There are different versions of the pen. I bought the Echo version due to the lower price. You can review the available pens on Amazon. I also bought additional Livescribe notebooks (they come in packs of four) and a portfolio (binder) to hold the notebook and pen.

My Experience with Livescribe

I have used a Livescribe pen for four years. After using to it to record hundreds of hours of audio, I consider my Livescribe pen to be one of my best audit tools. I recommend it.

What if you don’t desire to shell out the $155 for the pen? Consider using the Notability app.

Another Option

If you have an iPad, you can buy the Notability app for $9.99 and record conversations with your notes (with play-back similar to Livescribe). You will need a stylus (I use an Apple pen) to take notes since you write on your iPad screen. See my article about using Notability.

One More Thought

If you are performing a walkthrough of a complex transaction cycle, consider using your phone to take pictures of what you are seeing (e.g., computer screens, documents). I use the Scanbot app. Between your notes (with audio) and your pictures, you will have a good understanding of what you have seen and heard.

Are you preparing financial statements and wondering whether you need to include going concern disclosures? Or maybe you’re the auditor, and you’re wondering if a going concern paragraph should be added to the audit opinion. You’ve heard there are new requirements for both management and auditors, but you’re not sure what they are.

This article summarizes (in one place) the new going concern accounting and auditing standards.

Going Concern Standards

For many years the going concern standards were housed in the audit standards–thus, the need for FASB to issue accounting guidance (ASU 2014-15). It makes sense that FASB created going concern disclosure guidance. After all, disclosures are an accounting issue.

Going Concern Accounting Standard

ASU 2014-15, Disclosure of Uncertainties about an Entity’s Ability to Continue as a Going Concern, provides guidance in preparing financial statements. This standard was effective for years ending after December 15, 2016.

GASB Statement 56, Codification of Accounting and Financial Reporting Guidance Contained in the AICPA Statements on Auditing Standards, is the relevant going concern standard for governments. GASB 56 was issued in March 2009. (GASB 56 requires financial statement preparers to evaluate whether there is substantial doubt about a governmental entity’s ability to continue as a going concern for 12 months beyond the date of the financial statements. As you will see below, this timeframe is different from the one called for under ASU 2014-15. This post focuses on ASU 2014-15 and SAS 132.)

Meanwhile, the Auditing Standards Board issued their own going concern standard in February 2017: SAS 132.

Going Concern Auditing Standard

Auditors will use SAS 132, The Auditor’s Consideration of an Entity’s Ability to Continue as a Going Concern, to make going concern decisions. This SAS is effective for audits of financial statements for periods ending on or after December 15, 2017. SAS 132 amends SAS 126, The Auditor’s Consideration of an Entity’s Ability to Continue as a Going Concern.

So, let’s take a look at how to apply ASU 2014-15 and SAS 132.

Two Going Concern Decisions

In the past, the going concern decisions were made by auditors in a single step. Now, it is helpful to think of going concern decisions in two steps:

Management decisions concerning the preparation of financial statements

Auditor decisions concerning the audit of the financial statements

First, we’ll consider management’s decisions.

1. Management Decisions about Going Concern Accounting

ASU 2014-15 provides guidance concerning management’s determination of whether there is substantial doubt regarding the entity’s ability to continue as a going concern.

What is the Going Concern Accounting Definition?

FASB defines going concern with the words substantial doubt. So, how does FASB define substantial doubt?

Substantial doubt about the entity’s ability to continue as a going concern is considered to exist when aggregate conditions and events indicate that it is probable that the entity will be unable to meet obligations when due within one year of the date that the financial statements are issued or are available to be issued.

What is Probable?

So, how does management determine if “it is probable that the entity will be unable to meet obligations when due within one year”?

Probable means likely to occur.

If for example, a company expects to miss a debt service payment in the coming year, then substantial doubt exists. This initial assessment is made without regard to management’s plans to alleviate going concern conditions.

ASC 205-40-50-4 says:

The evaluation initially shall not take into consideration the potential mitigating effect of management’s plans that have not been fully implemented as of the date that the financial statements are issued (for example, plans to raise capital, borrow money, restructure debt, or dispose of an asset that have been approved but that have not been fully implemented as of the date that the financial statements are issued).

But what factors should management consider?

Factors to Consider

Management should consider the following factors when assessing going concern:

The reporting entity’s current financial condition, including the availability of liquid funds and access to credit

Obligations of the reporting entity due or new obligations anticipated within one year (regardless of whether they have been recognized in the financial statements)

The funds necessary to maintain operations considering the reporting entity’s current financial condition, obligations, and other expected cash flows

Other conditions or events that may affect the entity’s ability to meet its obligations

Moreover, management is to consider these factors for one year. But from what date?

Timeframe

The financial statement preparer (i.e., management or a party contracted by management) should assess going concern in light of one year from the date “the financial statements are issued or are available to be issued.”

So, if December 31, 2017, financial statements (for a nonpublic company) are available to be issued on March 15, 2017, the preparer looks forward one year from March 15, 2017. Then, the preparer asks, “Is it probable that the company will be unable to meet its obligations through March 15, 2018?” If yes, substantial doubt is present and disclosures are necessary. If no, then substantial doubt does not exist. As you would expect, the answer to this question determines whether going concern disclosures are to be made and what should be included.

Substantial Doubt Answer Determines Disclosures

If substantial doubt does not exist, then going concern disclosures are not necessary.

If substantial doubt exists, then the company needs to decide if management’s plans alleviate the going concern issue. This decision determines the disclosures to be made. The required disclosures are based upon whether:

Management’s plans alleviate the going concern issue

Management’s plans do not alleviate the going concern issue

What if Management’s Plans Alleviate the Going Concern Issue?

If conditions or events raise substantial doubt about an entity’s ability to continue as a going concern, but the substantial doubt is alleviated as a result of consideration of management’s plans, the entity should disclose information that enables users of the financial statements to understand all of the following (or refer to similar information disclosed elsewhere in the footnotes):

Principal conditions or events that raised substantial doubt about the entity’s ability to continue as a going concern (before consideration of management’s plans)

Management’s evaluation of the significance of those conditions or events in relation to the entity’s ability to meet its obligations

Management’s plans that alleviated substantial doubt about the entity’s ability to continue as a going concern

Management’s plans should be considered only if is it probable that they will be effectively implemented. Also, it must be probable that management’s plans will be effective in alleviating substantial doubt.

So, if management’s plans are expected to work, does the company have to explicitly state that management’s plans will alleviate substantial doubt? No.

When management’s plans alleviate substantial doubt, companies need not use the words going concern or substantial doubt in the disclosures. And as Sears discovered, it may not be wise to do so (their shares dropped 16% after using the term substantial doubt even though management had plans to alleviate the risk). Rather than using the term substantial doubt, consider describing conditions (e.g., cash flows are not sufficient to meet obligations) and management plans to alleviate substantial doubt.

The Company had losses of $4,525,123 in the year ending March 31, 2017. As of March 31, 2017, its accumulated deficit is $11,325,354.

Management believes the Company’s present cash flows will not enable it to meet its obligations for twelve months from the date these financial statements are available to be issued. However, management is working to obtain new long-term financing. It is probable that management will obtain new sources of financingthat will enable the Company to meet its obligations for the twelve-month period from the date the financial statements are available to be issued.

Notice this example does not use the words substantial doubt.

What if Management’s Plans Do Not Alleviate the Going Concern Issue?

If conditions or events raise substantial doubt about an entity’s ability to continue as a going concern, and substantial doubt is not alleviated after consideration of management’s plans, an entity should include a statement in the notes indicating that there is substantial doubt about the entity’s ability to continue as a going concern within one year after the date that the financial statements are available to be issued (or issued when applicable). Additionally, the entity should disclose information that enables users of the financial statements to understand all of the following:

Principal conditions or events that raise substantial doubt about the entity’s ability to continue as a going concern

Management’s evaluation of the significance of those conditions or events in relation to the entity’s ability to meet its obligations

Management’s plans that are intended to mitigate the conditions or events that raise substantial doubt about the entity’s ability to continue as a going concern

Sample Going Concern Disclosure – Substantial Doubt Not Alleviated

An example disclosure follows:

Note 2 – Going Concern

The financial statements have been prepared on a going concern basis which assumes the Company will be able to realize its assets and discharge its liabilities in the normal course of business for the foreseeable future. The Company had losses of $1,232,555 in the current year. The Company has incurred accumulated losses of $2,891,727 as of March 31, 2017. Cash flows used in operations totaled $555,897 for the year ended March 31, 2017.

Management believes these conditions raise substantial doubt about the Company’s ability to continue as a going concern within the next twelve months from the date these financial statements are available to be issued. The ability to continue as a going concern is dependent upon profitable future operations, positive cash flows, and additional financing.

Management intends to finance operating costs over the next twelve months with existing cash on hand and loans from its directors. Management is also working to secure new bank financing. The Company’s ability to obtain the new financing is not known at this time.

Notice this note includes a statement that substantial doubt is present. Though management’s plans are disclosed, the probability of success is not provided.

Going Concern Accounting Summary

ASU 2014-15 focuses on management’s assessment regarding whether substantial doubt exists. If substantial doubt exists, then disclosures are required. Here’s a short video summarizing 2014-15:

Thus far, we’ve addressed the stage 1. management decisions. As you can see management’s considerations focus on disclosures. By contrast, auditors focus on the audit opinion. Now, let’s look at what auditors must do.

2. Auditor Decisions Regarding Going Concern

SAS 132 provides guidance concerning the auditor’s consideration of an entity’s ability to continue as a going concern.

Auditing Going Concern Accounting

SAS 132, paragraph 10, states the objectives of the auditor are as follows:

Obtain sufficient appropriate audit evidenceregarding, and to conclude on, the appropriateness of management’s use of the going concern basis of accounting, when relevant, in the preparation of the financial statements

Conclude, based on the audit evidence obtained, whether substantial doubt about an entity’s ability to continue as a going concern for a reasonable period of time exists

Evaluate the possible financial statement effects, including the adequacy of disclosure regarding the entity’s ability to continue as a going concern for a reasonable period of time

Report in accordance with this SAS

These objectives can be summarized as follows:

Conclude about whether the going concern basis of accounting is appropriate

Determine whether substantial doubt is present

Determine whether the going concern disclosures are adequate

Issue an appropriate opinion

In light of these objectives, certain audit procedures are necessary.

Risk Assessment Procedures

In the risk assessment phase of an audit, the auditor should consider whether conditions or events raise substantial doubt. In doing so, the auditor should examine any preliminary management evaluation of going concern. If such an evaluation was performed, the auditor should review it with management. If no evaluation has occurred, then the auditor should discuss with management the appropriateness of using the going concern basis of accounting (the liquidation basis of accounting is required by ASC 205-30 when the entity’s liquidation is imminent) and whether there are conditions or events that raise substantial doubt.

The auditor is to consider conditions and events that raise substantial doubt about an entity’s ability to continue as a going concern for areasonable period of time. What is a reasonable period of time? It is the period of time required by the applicable financial reporting framework or, if no such requirement exists, within one year after the date that the financial statements are issued (or within one year after the date that the financial statements are available to be issued, when applicable). The governmental accounting standards require an evaluation period of “12 months beyond the date of the financial statements.”

Auditors should consider negative financial trends or factors such as:

Working capital deficiencies

Negative cash flows from operating activities

Default on loans

A denial of trade credit from suppliers

Need to restructure debt

Need to dispose of assets

Work stoppages or other labor problems

Need to significantly revise operations

Legal problems

Loss of key customers or suppliers

Uninsured catastrophes

The need for new capital

The risk assessment procedures are a part of planning an audit. You may obtain new information as you perform the engagement.

Remaining Alert Throughout the Audit

The auditor should remain alert throughout the audit for conditions or events that raise substantial doubt. So, after the initial review of going concern issues in the planning stage, the auditor considers the impact of new information gained during the subsequent stages of the engagement.

Audit Procedures When Substantial Doubt is Present

If events or conditions do give rise to substantial doubt, then the audit procedures should include the following (SAS 132, paragraph 16.):

Requesting management to make an evaluation when management has not yet performed an evaluation

Evaluating management’s plans in relation to its going concern evaluation, with regard to whether it is probable that:

management’s plans can be effectively implemented and

the plans would mitigate the relevant conditions or events that raise substantial doubt about the entity’s ability to continue as a going concern for a reasonable period of time

When the entity has prepared a cash flow forecast, and analysis of the forecast is a significant factor in evaluating management’s plans:

evaluating the reliability of the underlying data generated to prepare the forecast and

determining whether there is adequate support for the assumptions underlying the forecast, which includes considering contradictory audit evidence

Considering whether any additional facts or information have become available since the date on which management made its evaluation

Sometimes management’s plans to alleviate substantial doubt include financial support by third parties or owner-managers (usually referred to as supporting parties).

Financial Support by Supporting Parties

When financial support is necessary to mitigate substantial doubt, the auditor should obtain audit evidence about the following:

The intent of such supporting parties to provide the necessary financial support, including written evidence of such intent, and

The ability of such supporting parties to provide the necessary financial support

If the evidence in a. is not obtained, then “management’s plans are insufficient to alleviate the determination that substantial doubt exists.”

Intent of Supporting Parties

The intent of supporting parties may be evidenced by either of the following:

Obtaining from management written evidence of a commitment from the supporting party to provide or maintain the necessary financial support (sometimes called a “support letter”)

Confirming directly with the supporting parties (confirmation may be needed if management only has oral evidence of such financial support)

If the auditor receives a support letter, he can still request a written confirmation from the supporting parties. For instance, the auditor may desire to check the validity of the support letter.

If the support comes from an owner-manager, then the written evidence can be a support letter or a written representation.

Support Letter

An example of a third party support letter (when the applicable reporting framework is FASB ASC) is as follows:

(Supporting party name) will, and has the ability to, fully support the operating, investing, and financing activities of (entity name) through at least one year and a day beyond [insert date] (the date the financial statements are issued or available for issuance, when applicable).

You can specify a date in the support letter that is later than the expected date. That way if there is a delay, you may be able to avoid updating the letter.

The auditor should not only consider the intent of the supporting parties but the ability as well.

Ability of Supporting Parties

The ability of supporting parties to provide support can be evidenced by information such as:

Proof of past funding by the supporting party

Audited financial statements of the supporting party

Bank statements and valuations of assets held by a supporting party

After examining the intent and ability of supporting parties regarding the one-year period, you might identify potential going concern problems that will occur more than one year out.

Conditions and Events After the Reasonable Period of Time

So, should an auditor inquire about conditions and events that may affect the entity’s ability to continue as a going concern beyond management’s period of evaluation (i.e., one year from the date the financial statements are available to be issued or issued, as applicable)? Yes.

Suppose an entity knows it will be unable to meet its November 15, 2018, debt balloon payment. The financial statements are available to be issued on June 15, 2017, so the reasonable period goes through June 15, 2018. But management knows it can’t make the balloon payment, and the bank has already advised that the loan will not be renewed. SAS 132 requires the auditor to inquire of management concerning their knowledge of such conditions or events.

Why? Only to determine if any potential (additional) disclosures are needed. FASB only requires the evaluation for the year following the date the financial statements are issued (or available to be issued, as applicable). Events following this one year period have no bearing on the current year going concern decisions. Nevertheless, additional disclosures may be merited.

Thus far, the requirements to evaluate the use of the going concern basis of accounting and whether substantial doubt is present have been explained. Now, let’s see what the requirements are for:

Written representations from management

Communications with those charged with governance

Documentation

Written Representations When Substantial Doubt Exists

When substantial doubt exists, the auditor should request the following written representations from management:

A description of management’s plans that are intended to mitigate substantial doubt and the probability that those plans can be effectively implemented

That the financial statements disclose all the matters relevant to the entity’s ability to continue as a going concern including conditions and events and management’s plans

Communications with Those Charged with Governance

Remember that you may need to add additional language to your communication with those charged with governance.

When conditions and events raise substantial doubt about the entity’s ability to continue as a going concern for a reasonable period of time, the auditor should communicate the following (unless those charged with governance manage the entity):

Whether the conditions or events, considered in the aggregate, that raise substantial doubt about an entity’s ability to continue as a going concern for a reasonable period of time constitute substantial doubt

The auditor’s consideration of management’s plans

Whether management’s use of the going concern basis of accounting, when relevant, is appropriate in the preparation of the financial statements

The adequacy of related disclosures in the financial statements

The implications for the auditor’s report

Documentation Requirements

When substantial doubt exists before consideration of management’s plans, the auditor should document the following (SAS 132, paragraph 32.):

The conditions or events that led the auditor to believe that there is substantial doubt about the entity’s ability to continue as a going concern for a reasonable period of time.

The elements of management’s plans that the auditor considered to be particularly significant to overcomingthe conditions or events, considered in the aggregate, that raise substantial doubt about the entity’s ability to continue as a going concern, if applicable.

The audit procedures performed to evaluate the significant elements of management’s plans and evidence obtained, if applicable.

The auditor’s conclusion regarding whether substantial doubt about the entity’s ability to continue as a going concern for a reasonable period of time remains or is alleviated. If substantial doubt remains, the auditor should also document the possible effects of the conditions or events on the financial statements and the adequacy of the related disclosures. If substantial doubt is alleviated, the auditor should also document the auditor’s conclusion regarding the need for, and, if applicable, the adequacy of, disclosure of the principal conditions or events that initially caused the auditor to believe there was substantial doubt and management’s plans that alleviated the substantial doubt.

The auditor’s conclusion with respect to the effects on the auditor’s report.

Opinion – Emphasis of Matter Regarding Going Concern

If the auditor concludes that there is substantial doubt concerning the company’s ability to continue as a going concern, an emphasis of a matter paragraph should be added to the opinion.

An example of a going concern paragraph is as follows:

The accompanying financial statements have been prepared assuming that the Company will continue as a going concern. As discussed in Note 2 to the financial statements, the Company has suffered recurring losses from operations, has a net capital deficiency, and has stated that substantial doubt exists about the company’s ability to continue as a going concern. Management’s evaluation of the events and conditions and management’s plans regarding these matters are also described in Note 2. The financial statements do not include any adjustments that might result from the outcome of this uncertainty. Our opinion is not modified with respect to this matter.

The auditor should not use conditional language regarding the existence of substantial doubt about the entity’s ability to continue as a going concern.

Opinion – Inadequate Going Concern Disclosures

Paragraph 26. of SAS 132 states that an auditor should issue a qualified opinion or an adverse opinion, as appropriate, when going concern disclosures are not adequate.

Going Concern Auditing Summary

Now, let’s circle back to where we started and review the objectives of SAS 132.

The objectives are as follows:

Conclude about whether the going concern basis of accounting is appropriate

Determine whether substantial doubt is present

Determine whether the going concern disclosures are adequate

Issue an appropriate opinion

Conclusion

As you can see ASU 2014-15 and SAS 132 are complex. So, make sure you are using the most recent updates to your disclosure checklists and audit forms and programs.

Can you steal like a boss? White collar crime takes special skills and thoughts. Do you have what it takes? Here’s my tongue-in-cheek look at how I would steal.

Six Steps to Steal Like a Boss

To steal, I need to:

Be Believable

Have a Cause

Calm My Conscience

Develop My Plan

Execute My Plan

If Caught, Settle Out of Court

1. Be Believable

Look trustworthy. The more age, experience, and education I have, the better. The longer I work for the organization, the more I am trusted.

And while I’m at it, I’ll do what I can to move to positions of higher authority which will provide me with greater opportunities. Being in authority enables me to steal like a boss.

If possible, I will gain the ability to authorize or initiate purchases. Kickbacks (paid to those who authorize payments) are difficult to detect, even by professional fraud examiners, and the dollars can be significant. Like taking candy from a baby.

But before I steal, I need motivation.

2. Have a Cause

Any financial pressure will do–a gambling or drug habit, an affair, medical bills, or maybe I just want to appear more successful than I am. If I don’t have a need, I will create one. I am my own cause.

My unshareable need (cause) must not be known by others lest they suspect my need for cash.

One problem I must take care of before I steal is my conscience.

3. Calm My Conscience

I hate when that little voice starts talking: “Charles, you can’t do this. You’ll embarrass your wife.” It takes skill and fortitude, but I must calm my conscience. All the more reason to have a cause (see point 2.). The nobler I can make my reasons, the better. Something like, “I’ve earned this. The company should realize my greatness and provide me with appropriate compensation. I have three kids in college, and they need my support. You know I want to be a good provider for my family.”

I may need to start stealing borrowing or compensating myself in small amounts and then build up. Such wise reasoning will make it easier to calm my conscience.

Thinking correctly is important. When that little voice speaks, I will rephrase the words. I know I can. After all, I’ve done so for years.

Now I need to develop a plan.

4. Develop My Plan

I will pay attention to control weaknesses.

Our auditors have told us for years that we lack appropriate segregation of duties in regard to purchasing. Opportunity awaits.

If I am going to steal be compensated appropriately, I need to make it worth my while. Be bold. Think big. I have noticed that one of our key vendors has been very kind to me, a free week-long trip to Vegas for the last three years.

A key contract renewal is coming up. The vendor should be more generous to me. Besides, last year the CFO received a nicer trip than I did (two weeks in Austria). And bribes gifts don’t hurt anyone; the vendor pays for them (though I have noticed the vendor’s pricing seems to be increasing…actually, exploding).

It’s game time. I need to “just do it.” But how?

5. Execute My Plan

Take I must compensate myself in a steady under-the-radar kind of way. Most folks get greedy. I must be diligent to work in a measured way, not taking receiving noticeable amounts. Greed is my enemy. Excess might land me on the front page of the paper.

Also, I think I can steal borrow money from the receipts cycle since I am in charge of daily deposits and all related accounting duties. This might cost me my vacation though. I need to be on the job to continue to hide perform my duties. But if the funds taken compensation is enough, it might be worth it.

But what if my actions become known to others?

6. If I Get Caught, Settle Out of Court

If I am discovered someone notices that I have borrowed funds, then I may have to beg for forgiveness and promise to pay it back. And, of course, I need to make sure the company understands my concern for its reputation. News like this does not support the company’s mission statement: Honesty and Compassion for Those We Serve.

I don’t need a criminal record, especially if I need to steal borrow funds from my next employer. It is comforting to know that in many cases companies don’t prosecute for fear of public embarrassment.

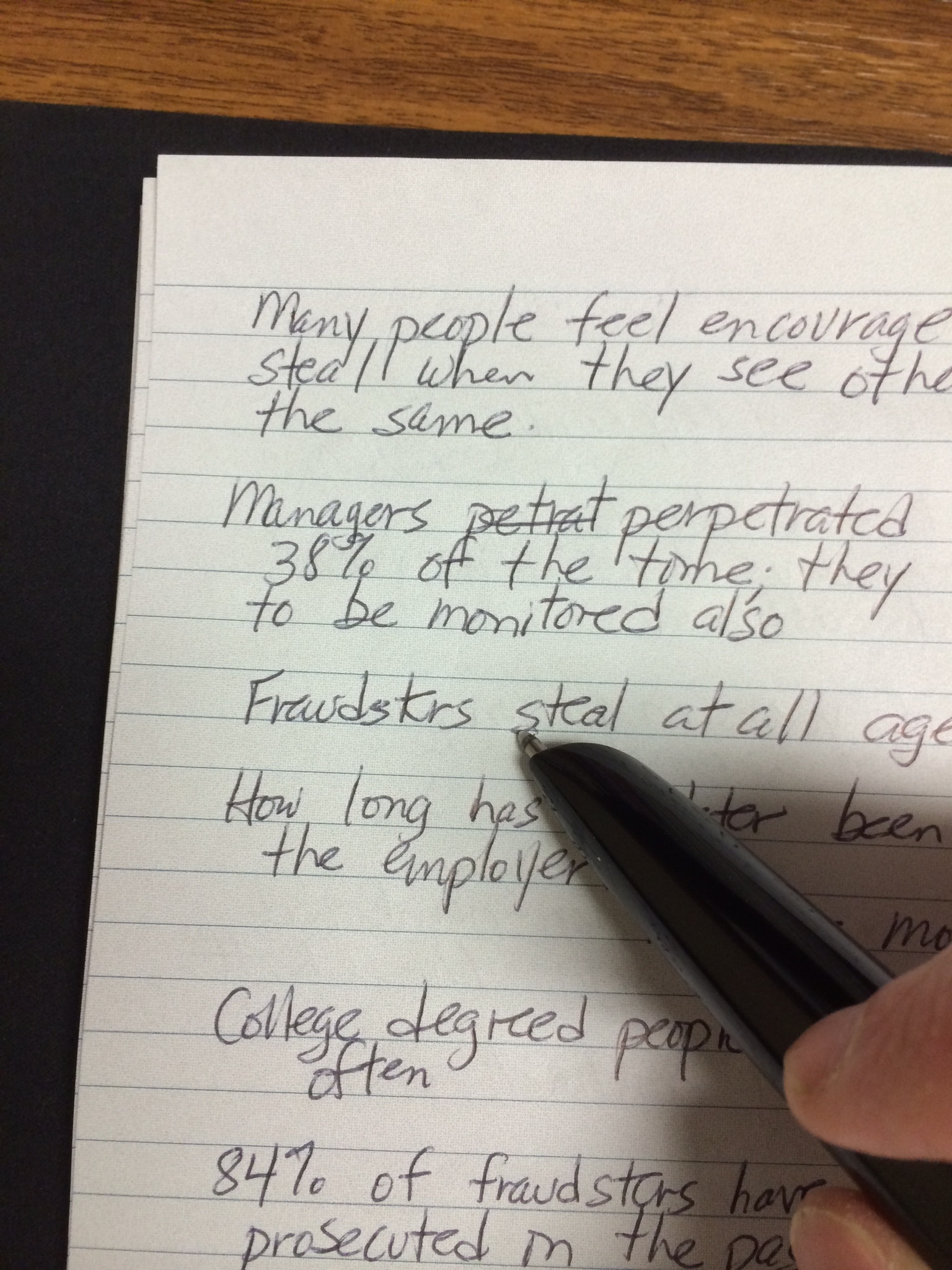

Here are key findings from the 2018 ACFE Fraud Report. The survey is titled the 2018 Report to the Nations.

Every two years the Association of Certified Fraud Examiners (ACFE) issues a fraud report based on hundreds of actual fraud cases. The report provides great insights into how fraud occurs (the method), the persons stealing (the fraudster), and the damage (the amount of losses).

If you are an auditor (internal or external), then you need to be familiar with the findings in this report. Understanding how theft occurs will enable you to detect and prevent it in the future.

The median loss per case when owners or executives were involved was $850,000

Businesses with a 100 or fewer employees suffered a median loss per case of $200,000

Businesses with more than 100 employees suffered a median loss per case of $104,000

In 40% of the cases, tips were the initial detection method (53% of the tips came from employees of the organization; 32% of the tips came from vendors, customers, and competitors)

Fraud losses were 50% smaller for organizations with fraud hotlines

Only 4% of the fraudsters had a prior fraud conviction

Occupational fraud was committed in the following categories: (1) asset misappropriation (89%), (2) corruption (38%), and (3) financial statement fraud (10%) -- in some cases, the fraudster used multiple schemes

The median losses were (1) $114,ooo for asset misappropriation, (2) $250,000 for corruption, and (3) $800,000 for financial statement fraud

70% of corruption cases were committed by someone in a position of authority

82% of corruption cases were committed by males

50% of corruption cases were detected by a tip

Internal control weaknesses led to nearly half of the fraud

Small businesses typically have fewer anti-fraud controls than larger organizations, leaving them more vulnerable

Data monitoring/analysis and surprise audits were correlated with the largest reductions in fraud losses and duration (yet only 37% of victim organizations implemented these controls)

A majority of the victim organizations recovered nothing

Fraudsters that were with the company for more than five years stole an average of $200,000

Fraudsters that were with a company for less than five years stole an average of $100,000

The industries with the highest levels of fraud were (1) Banking and Financial, (2) Manufacturing, (3) Governments, and (4) Health Care

The departments with the highest level of fraud were (1) Accounting (14%), (2) Operations (14%), (3) Sales (12%), and (4) Executive/upper management (11%)

69% of frauds were commented by males with a median loss of $156,000 (the median loss from female thefts was $89,000)

61% of the fraud cases involved someone with a university degree or postgraduate degree

When one fraudster was involved, the median loss was $74,000

When two fraudsters were involved, the median loss was $150,000

When three or more fraudsters were involved, the median loss was $339,000

Living beyond their means was the primary behavioral red flag (41% of cases)

I have been a member of the Association of Certified Fraud Examiners since 2004. Why? Because I want to be a better auditor. And I have found that the ACFE has given me a much greater understanding of how fraud happens and how to prevent it. The organization has made me a much better auditor. Consider joining this organization. (You can join without becoming a Certified Fraud Examiner (CFE), though I recommend doing that as well. Learn more about becoming a CFE.) You'll be glad you did.