What financial statement references are required at the bottom of financial statement pages? Is there a difference in the references in audited statements and those in compilations or reviews? What wording should be placed at the bottom of supplementary pages? Below I answer these questions.

Audited Financial Statements and Supplementary Information

First, let’s look at financial statement references in audit reports.

While generally accepted accounting principles do not require financial page references to the notes, it is a common practice to do so. Here are examples:

See notes to the financial statements.

The accompanying notes are an integral part of these financial statements.

See accompanying notes.

Accountants can also–though not required–reference specific disclosures on a financial statement page. For example, See Note 6 (next to the Inventory line on a balance sheet). It is my preference to use general references such as See accompanying notes.

Audit standards do not require financial statement page references to the audit opinion.

Supplementary pages should not include a reference to the notes or the opinion.

The Statements on Standards for Accounting and Review Services (SSARS) do not require a reference (on financial statement pages) to the compilation or review report; however, it is permissible to do so. What do I do? I do not refer to the accountant’s report. I include See accompanying notes at the bottom of each financial statement page (when notes are included). This reference to notes, however, is not required, even when notes are included. (Notes can be omitted in compilation engagements.)

You are not required to include a reference to the accountant’s report on the supplementary information pages. Examples include:

See Accountant’s Compilation Report.

See Independent Accountant’s Review Report.

What do I do? I include a reference to the accountant’s report on each supplementary page. But, again, it’s fine to not include a reference to the report.

Preparation of Financial Statement Engagements

Additionally, SSARS provides a nonattest option called the preparation of financial statements (AR-C 70). This option is used by the CPA to issue financial statements that are not subject to the compilation standards. No compilation report is issued. AR-C 70 requires that the accountant either state on each page that “no assurance is provided” or provide a disclaimer that precedes the financial statements. AR-C 70 does not require that the financial statement pages refer to the disclaimer (if provided), but it is permissible to do so. Such a reference might read See Accountant’s Disclaimer.

If your AR-C 70 work product has supplementary information, consider including this same reference (See Accountant’s Disclaimer) on the supplementary pages.

Which standards apply when you prepare financial statements?

The AICPA Accounting and Review Services Committee added a section to the compilation and review standards called Preparation of Financial Statements. Since then, I’ve received several questions about which standards apply when financial statements are prepared–especially if you concurrently provide another service such as a compilation, review, or audit.

Those questions include:

Can an accountant perform a compilation and not prepare the financial statements?

Are the preparation of financial statements and the performance of a compilation engagement two separate services?

If an auditor prepares financial statements and audits a company, what is the relevant standard for preparing the financial statements?

Is the preparation of financial statements a nonattest service, though the audit is an attest service?

Below I provide: (1) a summary of how compilations changed with the issuance of SSARS 21 and (2) a summary of how the preparation of financial statements service interplays with compilations, reviews, and audits.

The Old Compilation Standard

Using SSARS 19, the performance of a compilation involved one service which encompassed:

Preparing financial statements,

Performing compilation procedures (e.g., reading the financials), and

Issuing a report

How Compilation Engagements Changed

So, how did SSARS 21 change compilations?

If an accountant prepares the financial statements and performs a compilation engagement using SSARS 21, she is performing two services (not one). In this case, the performance of the preparation of financial statements is not subject to any formal standard (including SSARS 21).

When an accountant performs both the preparation of financial statements and a related compilation engagement, is AR-C 70, Preparation of Financial Statements, applicable?

No.

“Wait…you’re saying that a new standard called Preparation of Financial Statements was added with SSARS 21, but when the accountant prepares financial statements and performs a compilation engagement, the (SSARS 21) preparation standard is not applicable?”

Yes.

AR-C 70, Preparation of Financial Statements, states that the standard is not applicable “when an accountant prepares financial statements and is engaged to perform an audit, review, or compilation of those financial statements.” So if an accountant prepares financial statements as a part of a compilation engagement, AR-C 70 does not apply.

Why?

If AR-C 70, Preparation of Financial Statements, and AR-C 80, Compilation Engagements, were both in play, they would conflict. AR-C 70 requires the accountant to state on each financial statement page that “no assurance is provided” or to issue a disclaimer. AR-C 80 requires the issuance of a compilation report and does not allow the accountant to state that “no assurance is provided” on each financial statement page or for the accountant to issue a disclaimer.

Meaning?

When the accountant prepares financial statements and performs a related compilation, the creation of the financial statements is a nonattest service with no particular guidance–not even from SSARS 21. (Of course, the AICPA Code of Professional Conduct applies to all services.)

When a compilation engagement (an attest service) is performed and financial statements are prepared (a nonattest service), two separate services are being performed by the same accounting firm.

Financial Statement Preparation and Other Services

The table summarizes which standard is applicable when:

1. A preparation engagement is performed (alone)

2. Preparation and compilation engagements are performed for the same time period

3. Preparation and review engagements are performed for the same time period

4. Preparation and audit engagements are performed for the same time period

Preparation of Financial Statements

Compilation Engagement

Review Engagement

Audit Engagement

Standard to Follow

Yes

AR-C 70 Preparation

Yes

Yes

AR-C 80 Compilation

Yes

Yes

AR-C 90 Review

Yes

Yes

AU-C Audit Sections

AR-C 70, Preparation of Financial Statements, applies only in the first example above. When the accountant performs a preparation service and a compilation, review, or audit service for the same time period, AR-C 70 is not applicable–that is, no formal standard applies to the preparation service.

In all the examples listed above, the preparation of financial statements is a nonattest service.

In examples 2, 3 and 4 (where a preparation service and an attest service are provided), your engagement letter should include language about performing nonattest services and how the client will assign someone with suitable skill, knowledge, and experience to oversee the preparation of financial statements service. Such language is only required when a nonattest and an attest service is provided.

SSARS 22 and 23

Since the above information deals with SSARS 21, you may be wondering what additional SSARS have been issued–and how those newer standards affect compilations.

SSARS 22, Compilation of Pro Forma Financial Information was effective for compilation reports dated on or after May 1, 2017. So, what is pro forma information? It is a presentation that shows what the significant effects on historical financial information might have been had a consummated or proposed transaction (or event) occurred at an earlier date.

The primary impact of SSARS 23 is to provide standards for the preparation and compilation of prospective financial information.

While portions of SSARS 23 were effective upon issuance (the supplementary language change), the remainder of the standard was effective for prospective financial information prepared on or after May 1, 2017, and for compilation reports dated on or after May 1, 2017, respectively.

SSARS 21 has been in existence since October 2014. What have we learned about this standard?

(SSARS 22 and SSARS 23 were subsequently added, but most of the SSARS 21 guidance remains as originally issued.)

Preparation of Financial Statements or Compilation Reports

Before SSARS 21, if an accountant created financial statements and submitted them to a client, he had to issue a compilation report. Now, using the Preparation of Financial Statements part of SSARS 21 (AR-C 70), an accountant can create and provide financial statements without a compilation report. Such financial statements can be provided to third parties such as banks–again with no compilation report. So, how have accountants responded to the option to provide financial statements to clients without a compilation report?

It has been my observation that many accountants continue to perform compilation engagements (rather than use the preparation option). Why? I think we are creatures of habit. We have issued compilation reports for so long that we’re comfortable doing so–and we continue to do the same. Also, as we’ll see in a minute, performing a compilation doesn’t take much additional time.

Some accountants, however, are using AR-C 70. They are issuing financial statements without a compilation report and stating that “no assurance is provided” on each page–or, as the standard allows, placing a disclaimer page in front of the financial statements.

Who Should Use the Preparation Standard?

So, who uses AR-C 70? Accountants with limited time.

Suppose, for example, that a client wants a balance sheet and nothing else. You can create the balance sheet in Excel and put “no assurance is provided” at the bottom of the page. And you’re done–with the exception of obtaining a signed engagement letter. (Accountants should document any significant consultations or professional judgments, but usually, there are none.)

Can I Avoid the Engagement Letter?

You may be thinking, “Charles, I’m not sure I’m saving much time if I have to create an engagement letter. Getting a signed engagement letter might even take more time than preparing the balance sheet.” Yes, that is true. So, is there a situation where the engagement letter is not required? Yes, sometimes.

Financial Statements as a Byproduct

You can provide the balance sheet to a client without obtaining an engagement letter if the statement preparation is a byproduct of another service (as long as you have not been engaged to prepare the financial statement). For example, if you’re preparing a tax return and create the balance sheet as a byproduct of the tax service, you are not required to obtain a SSARS engagement letter? Why? Because you have not been engaged to prepare the financial statement. The trigger for AR-C 70 is whether you have been engaged to prepare financial statements.

QuickBooks Bookkeeping

The same is true if you provide bookkeeping services using QuickBooks in the Cloud. If you have not been engaged to prepare financial statements and the online software allows you to print the financial statements, you are not in the soup. That is, you are not following AR-C 70–because you have not been engaged to prepare financial statements. If your client asks you to perform bookkeeping service in a cloud-based accounting package (such as QuickBooks) and to prepare financial statements, you are engaged. Then you must follow AR-C 70 and obtain an engagement letter–and follow the other requirements of the standard.

In most compilations, the accountant prepares the financial statements and performs the compilation engagement. Notice these are two different services: (1) preparing the financial statements and (2) performing the compilation. It is possible for your client to create the financial statement and for you (the accountant) to perform the compilation, though this is rare. If you do both, the preparation of financial statements is not performed using AR-C 70. So what standard should you follow for the preparation of the financial statements. There is none. You are just performing a nonattest service. Then you’ll perform the compilation engagement using AR-C 80.

So, the question at this point is whether you should prepare financial statements using AR-C 70 or create the financial statements and perform a compilation using AR-C 80. (Technically, the choice is the clients, but you are explaining the differences to them.)

Additional Time for Compilations

How much extra time does it take to perform a compilation engagement after the financial statements are created? Not much. You are only placing a compilation report on your letterhead (rather than stating that “no assurance is provided” on each page or providing a disclaimer that precedes the financial statements).

What other procedures are required for a compilation (versus providing the financial statements under AR-C 70)? You are reading the financial statements to see if they are appropriate. And since you just created the statements, that shouldn’t take much time.

Regardless, both AR-C 70 and AR-C 80 require signed engagement letters. So if you’ve been engaged to prepare financial statements or perform a compilation, there is no getting around the requirement for an engagement letter.

Is a Preparation or a Compilation Service Best?

So which is better? Using AR-C 70 (Preparation of Financial Statements) or AR-C 80 (Compilation Engagements)? It depends.

Some banks desire a compilation report, so in that case, of course, you are going to–at the request of the client–perform a compilation engagement.

Also, some CPAs feel safer issuing a compilation report that spells out (in greater detail than a preparation disclaimer) what is done and what is not done. We don’t know yet whether a preparation service creates greater legal exposure than a compilation. But we will with time. After a few years of using SSARS 21, I think our insurance companies will tell us whether one service creates more exposure than another. So far, I have not seen any such studies. Why? SSARS 21 has been in use only a couple of years.

Another factor to consider is peer review. The AICPA standards do not require a peer review if you only provide financial statements using AR-C 70. But check with your state board of accountancy; some states require peer review, regardless.

For the most efficient way to issue financial statements, click here.

SSARS 23 changes preparation and compilation engagements. The article summarizes the effects of the new standard.

The Accounting and Review Services Committee (ARSC) issued SSARS 23 in October 2016. Parts of the standard (e.g., that applying to supplementary information language in compilation and review reports) were effective immediately. Other parts (mainly regarding preparation and compilation of prospective information) are required as of May 1, 2017. This post tells you how SSARS 23 affects Preparation (AR-C 70) and Compilation (AR-C 80) engagements.

You’ll recall that ARSC issued SSARS 21 back in October 2014. It was effective for years ending December 31, 2015. A clarified version of the compilation and review standards is included in SSARS 21. SSARS 21 also provides new guidance for the preparation of financial statements. The Standard did not address prospective financial statements. Why? The AICPA was working on clarifying the Attestation Standards (SSAE 18), the place where compiled prospective financial statement guidance was (previously) housed. With the issuance of SSARS 23, the AICPA moved this guidance from the Attestation Standards to SSARS.

The primary impact of SSARS 23 is to provide standards for the preparation and compilation of prospective financial information.

How Preparation of Financial Statements (AR-C 70) Changed

The Preparation Standard (AR-C 70) now includes guidance regarding prospective financial information. SSARS 23 requires the inclusion of significant assumptions since they are essential to understanding prospective information. Therefore, accountants should not prepare prospective financial information without including a summary of significant assumptions in the notes. Also, a financial projection should not be created unless it includes:

an identification of the hypothetical assumptions, or

a description of the limitations on the usefulness of the presentation

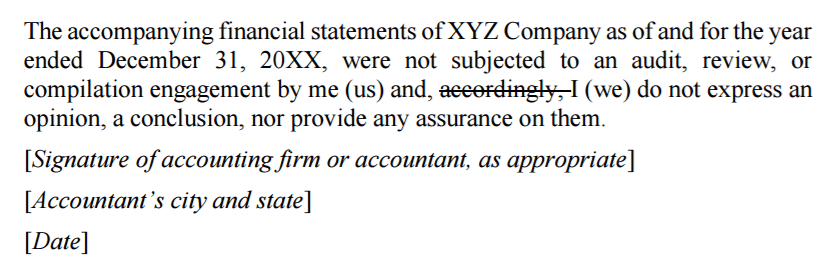

One other change to AR-C 70 is the slight change to the preparation disclaimer. SSARS 23 deletes the word “accordingly.” See below:

How Compilation Engagements (AR-C 80) Changed

AR-C 80, Compilation Engagements, now applies to compilations of prospective financial information (new with SSARS 23), pro forma financial information (see SSARS 22), and other historical information (as provided for in SSARS 21).

Another change is that accountants should report known departures from the applicable financial reporting framework in the compilation report. Prior to SSARS 23, accountants could disclose such departures in the notes without doing so in the compilation report.

Prospective Financial Information Guidance

Additionally, AR-C 70 and AR-C 80 were amended to clarify that the AICPA Guide Prospective Financial Information provides comprehensive guidance regarding prospective financial information, including suitable criteria for the preparation and presentation of such information.

Are you wondering how to present supplementary information in compilation and preparation engagements? What supplementary information (SI) should be included? How does the accountant define his or her responsibility for SI?

Often accountants, at the request of their clients, add supplementary information to the financial statements. Such information is never required (to be in compliance with a reporting framework) but may be useful.

You can think of financials with supplementary information in this manner:

Financial statements – Required – The jeep in the picture above

Supplementary Information – Not required – The camper

You’re not going anywhere without a vehicle (it’s required). And your camper (not required) is no good without an automobile to pull it. Kind of a silly analogy, I know, but maybe it will help you remember.

I normally add a divider page between the financial statements and supplementary information (though such as page is not required); the divider page simply says “Supplementary Information” and nothing else.

SSARS 21 defines supplementary information as follows:

Information presented outside the basic financial statements, excluding required supplementary information, that is not considered necessary for the financial statements to be fairly presented in accordance with the applicable financial reporting framework.