Menu

SSARS 23 changes preparation and compilation engagements. The article summarizes the effects of the new standard.

The Accounting and Review Services Committee (ARSC) issued SSARS 23 in October 2016. Parts of the standard (e.g., that applying to supplementary information language in compilation and review reports) were effective immediately. Other parts (mainly regarding preparation and compilation of prospective information) are required as of May 1, 2017. This post tells you how SSARS 23 affects Preparation (AR-C 70) and Compilation (AR-C 80) engagements.

You’ll recall that ARSC issued SSARS 21 back in October 2014. It was effective for years ending December 31, 2015. A clarified version of the compilation and review standards is included in SSARS 21. SSARS 21 also provides new guidance for the preparation of financial statements. The Standard did not address prospective financial statements. Why? The AICPA was working on clarifying the Attestation Standards (SSAE 18), the place where compiled prospective financial statement guidance was (previously) housed. With the issuance of SSARS 23, the AICPA moved this guidance from the Attestation Standards to SSARS.

The primary impact of SSARS 23 is to provide standards for the preparation and compilation of prospective financial information.

The Preparation Standard (AR-C 70) now includes guidance regarding prospective financial information. SSARS 23 requires the inclusion of significant assumptions since they are essential to understanding prospective information. Therefore, accountants should not prepare prospective financial information without including a summary of significant assumptions in the notes. Also, a financial projection should not be created unless it includes:

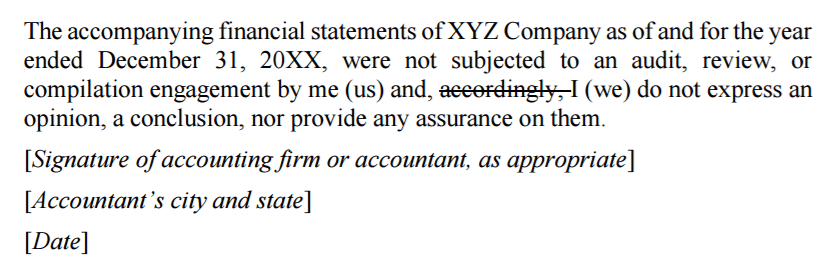

One other change to AR-C 70 is the slight change to the preparation disclaimer. SSARS 23 deletes the word “accordingly.” See below:

AR-C 80, Compilation Engagements, now applies to compilations of prospective financial information (new with SSARS 23), pro forma financial information (see SSARS 22), and other historical information (as provided for in SSARS 21).

Another change is that accountants should report known departures from the applicable financial reporting framework in the compilation report. Prior to SSARS 23, accountants could disclose such departures in the notes without doing so in the compilation report.

Additionally, AR-C 70 and AR-C 80 were amended to clarify that the AICPA Guide Prospective Financial Information provides comprehensive guidance regarding prospective financial information, including suitable criteria for the preparation and presentation of such information.

Charles Hall is a practicing CPA and Certified Fraud Examiner. For the last thirty-five years, he has primarily audited governments, nonprofits, and small businesses. He is the author of The Little Book of Local Government Fraud Prevention, The Why and How of Auditing, Audit Risk Assessment Made Easy, and Preparation of Financial Statements & Compilation Engagements. He frequently speaks at continuing education events. Charles consults with other CPA firms, assisting them with auditing and accounting issues.

Session expired

Please log in again. The login page will open in a new tab. After logging in you can close it and return to this page.

Chuck, sorry but I haven’t taken any write up or compilation CPE in while. I teach compilation and review classes to my firm and get credit that way. Sorry but I don’t offer any online CPE classes.

I need to pick up dome CPE for write up & comp, any suggestions?