Charles Hall is a practicing CPA and Certified Fraud Examiner. For the last thirty-five years, he has primarily audited governments, nonprofits, and small businesses.

He is the author of The Little Book of Local Government Fraud Prevention, The Why and How of Auditing, Audit Risk Assessment Made Easy, and Preparation of Financial Statements & Compilation Engagements. He frequently speaks at continuing education events.

Charles consults with other CPA firms, assisting them with auditing and accounting issues.

Do you struggle with what needs to be done in an audit–and what does not? Do you perform audit procedures (because they are in a standard audit program) but you’re not sure why? Do you ever feel like your audit will never end? You are not alone.

While audit forms—like risk assessment, audit planning, and audit program—are necessary, they can make us feel like a blind man being led by the hand. If you’re like me, you want to see, to know where you’re going and why. To gain sight, we need to go back to the basics.

Each year, Vince Lombardi (the revered coach of the Green Bay Packers) held a pigskin up and said, “This is a football.” And he did so with the best players in the world. He knew that winning is all about basics: blocking, tackling, passing, running. Understanding fundamentals brings clarity and power. And that’s what I’m after in The Why and How of Auditing. I’ll strip away the technical mumbo-jumbo and make auditing accessible, even for beginners. Moreover, experienced auditors will profit as you revisit what matters (and what does not).

In the cartoons I read as a kid, Lucy would say to Charlie Brown, “I will hold the ball, and you kick,” but as Charlie Brown would lean into his launch, she would pull away. And you remember the result: Charlie Brown, lying on his backside.

Some audit procedures (like the invitation to kick) are tempting. They call us (like a familiar friend), but they are a waste of time–even if we have done these steps for years. In the end, they leave us staring at the sky. So, we need to know what is best and what is necessary. Then, we can avoid waste.

This series provides you with what you need to know—without excess baggage. By design, the series is simple. Why? To provide clarity. I want you to understand the basics of auditing.

When you’re done, you’ll understand auditing, possibly in a way you never have. Then you’ll work with greater confidence and effectiveness. So, let’s begin.

Do you ever need a heavy-weight to assist you with a complex accounting issue? Or do you ever wonder how you’ll ever keep up with all the new FASB and AICPA standards? The Center for Plain English Accounting (CPEA) might be your answer.

Last week I was working with another partner to resolve a nonprofit accounting issue. He had one opinion and I had another. Both were logical. Each appeared to be possible. But we needed a single answer. What did we do? We submitted our question to the CPEA. Within twenty-four hours we had an answer–in writing. (I would say who was right but I might embarrass myself.) And with it, we documented our consultation per our firm’s quality control document. Now, if the issue comes up in peer review, we have a solid answer for our position.

Below I provide you with a review of the CPEA and whether the annual dues are worthwhile.

Why Join the Center for Plain English Accounting?

My firm joined the CPEA about four years ago. What led to that decision? We had used the free AICPA Hotline service for years, and the experience was positive. But as you may know, the AICPA Hotline does not offer written responses. I would send the Hotline an email with an inquiry, and the AICPA would call me with an answer, usually within 24 hours. I would document that discussion in my engagement file. But, in the back of my mind, Ialways longed for a written response. Why? These were usually thorny, high-risk issues. And I wanted black-and-white written answers. Something I could bank on. This is part of what the CPEA does: they provide written answers to technical questions.

Center for Plain English Accounting Mission

The CPEA provides other services as well.

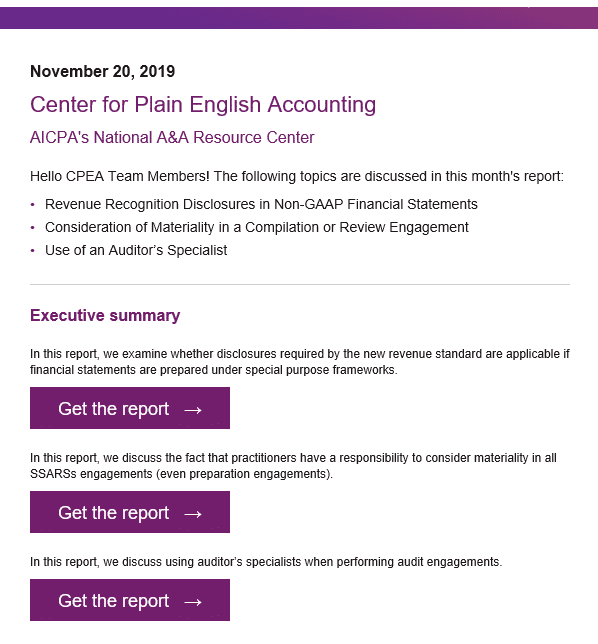

As a member, you receive a monthly report (see example below) covering a variety of accounting and auditing issues. You also receive emails with alerts and special reports about hot-topic issues. The last alert informed members about the delay in the effective date of the lease standard. These technical reports and alerts are accessible online, so you have a library of past articles to assist you.

Here’s my latest monthly special report email.

Additionally, the CPEA offers CPE at reasonable rates. These are online sessions, though they do offer an in-house option.

In short, the CPEA provides information about evolving technical issues and answers to specific accounting and auditing questions.

I have found their staff to be accessible and easy to work with. They are some of the best in the business.

Here’s an excerpt from their website regarding what they do:

The Center for Plain English Accounting (CPEA) is the AICPA’s national A&A resource center, sponsored by the Private Companies Practice Section. The CPEA’s team of experts assist members with accounting, auditing, attest, review, and compilation needs by sharing technical advice and guidance. The CPEA’s straight-forward and clear style of writing and speaking gives practitioners the opportunity to understand the applicability of the professional literature when preparing financial statements and when auditing, reviewing, and compiling those financial statements.

Cost of CPEA Membership

What’s the cost of joining the CPEA? $1,700 per year. So it’s not cheap. But I feel like my company receives its money’s worth. We pose several questions each year, and we receive timely written responses–every time. For firms that don’t have a national office (and most don’t), this is an excellent solution.

There are also smaller firm options. If you have five or fewer professionals, the annual fee is $795. If you are a sole practitioner, it is $450. Additionally, if you are not a member, you can pay a per-inquiry fee of $300.

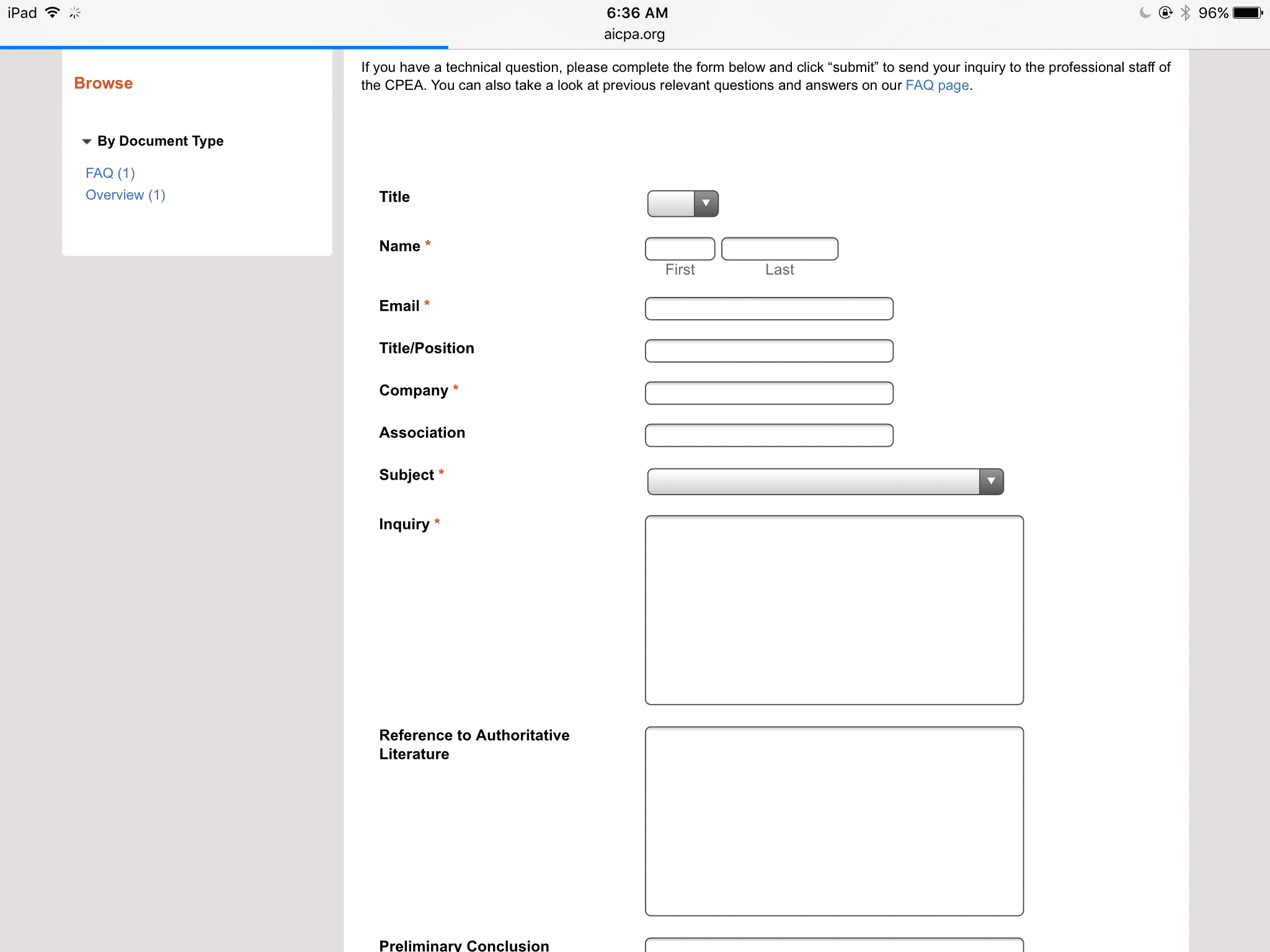

How do you submit your questions to the CPEA? With an online form such as the following:

Worth the Money?

For me, the cost of membership has been worth the money. If your firm desires to keep up with evolving standards and needs written answers to technical questions, the CPEA is an excellent choice.

How does a debt covenant violation affect the presentation of debt on a balance sheet? If a waiver from the lender is obtained, should the violation be disclosed? In this article, I will tell you how to report debt covenant violations.

Lenders commonly include debt covenants in loan agreements. Those covenants might require certain profitability, liquidity, or cash flow ratios. A violation of such requirements can make long-term debt callable. And, by definition, the debt becomes current since it is now due within one year of the balance sheet date.

If a debt covenant violation occurs, the debt should be classified as current unless the lender provides a waiver for more than one year from the balance sheet date. (See an exception below when there are subsequent measurement dates within one year of the balance sheet date.)

How should debt be classified if a cure occurs prior to the issuance of the financial statements? Debt is shown as noncurrent if the company is able to cure a violation subsequent to the balance sheet date but before the issuance date (or date available for issuance) of the financial statements.

Additionally, some loans provide for a grace period. If the violation is cured during the grace period, the debt will be reported as long-term. Also if the cure has not already occurred but the company demonstrates it is probable that the cure will occur within the grace period, then the debt will be reported as long-term.

Reporting Debt Covenant Violations

When a violation occurs, the main consideration in classifying long-term debt is whether the amount is due or callable within one year of the balance sheet date. If the loan is due or callable within the year after the period-end, the amount generally should be reported as current. If a debt covenant violation is timely cured within a grace period, then the debt is no longer callable and will, therefore, remain long-term. Noncurrent classification is also appropriate if the creditor provides a waiver that extends more than one year beyond the balance sheet date.

Waivers do not, however, guarantee long-term debt classification, particularly if there are other measurement dates within the year after the period-end.

Subsequent Measurement Dates

470-10-45 of the FASB Codification provides the following guidance:

Some long-term loans require compliance with quarterly or semiannual covenants that must be met on a quarterly or semiannual basis. If a covenant violation occurs that would otherwise give the lender the right to call the debt, a lender may waive its call right arising from the current violation for a period greater than one year while retaining future covenant requirements. Unless facts and circumstances indicate otherwise, the borrower shall classify the obligation as noncurrent, unless both of the following conditions exist:

a. A covenant violation that gives the lender the right to call the debt has occurred at the balance sheet date or would have occurred absent a loan modification. b. It is probable that the borrower will not be able to cure the default (comply with the covenant) at measurement dates that are within the next 12 months.

If both of these conditions exist, then the debt is shown as current.

Consider a scenario where a company has a covenant violation on December 31, 2019, and it obtains a waiver from the lender that lasts through January 1, 2021. If a September 30, 2020 measurement date is required by the loan agreement and it is probable that the company will not be in compliance, then the loan is classified as current on December 31, 2019, even though the waiver was obtained. Why? The new violation would make the loan callable within one year of the balance sheet date. (The prior waiver was in relation to the December 31, 2019 violation, not a subsequent violation.)

Is Disclosure Required if a Waiver is Obtained?

If a company obtains a waiver for more than one year from the balance sheet date, must the financials disclose this fact (that a waiver was obtained)?

The AICPA answers this question–in Q&A section 3200 (paragraph 17)–with the following:

The authoritative literature applicable to nonpublic entities does not address disclosure of debt covenant violations existing at the balance-sheet date that have been waived by the creditor for a stated period of time. Nevertheless, disclosure of the existing violation(s) and the waiver period should be considered* for reasons of adequate disclosure. If the covenant violation resulted from nonpayment of principal or interest on the debt, inability to maintain required financial ratios or other such financial covenants, that information may be vital to users of the financial statements even though the debt is not callable.

*Emphasis added by CPAHallTalk

Translation: It is wise to disclose the debt covenant violation and the existence of the waiver.

FASB’s Current Work on a New Debt Standard

The FASB has an ongoing project regarding the classification of debt. The FASB issued a revised Exposure Draft on September 12, 2019, Debt (Topic 470): Simplifying the Classification of Debt in a Classified Balance Sheet (Current versus Noncurrent). Comments were due October 28, 2019. It has taken FASB over two years to deliberate this topic. So you call tell the classification decision is not an easy one.

What financial statement references are required at the bottom of financial statement pages? Is there a difference in the references in audited statements and those in compilations or reviews? What wording should be placed at the bottom of supplementary pages? Below I answer these questions.

Audited Financial Statements and Supplementary Information

First, let’s look at financial statement references in audit reports.

While generally accepted accounting principles do not require financial page references to the notes, it is a common practice to do so. Here are examples:

See notes to the financial statements.

The accompanying notes are an integral part of these financial statements.

See accompanying notes.

Accountants can also–though not required–reference specific disclosures on a financial statement page. For example, See Note 6 (next to the Inventory line on a balance sheet). It is my preference to use general references such as See accompanying notes.

Audit standards do not require financial statement page references to the audit opinion.

Supplementary pages should not include a reference to the notes or the opinion.

The Statements on Standards for Accounting and Review Services (SSARS) do not require a reference (on financial statement pages) to the compilation or review report; however, it is permissible to do so. What do I do? I do not refer to the accountant’s report. I include See accompanying notes at the bottom of each financial statement page (when notes are included). This reference to notes, however, is not required, even when notes are included. (Notes can be omitted in compilation engagements.)

You are not required to include a reference to the accountant’s report on the supplementary information pages. Examples include:

See Accountant’s Compilation Report.

See Independent Accountant’s Review Report.

What do I do? I include a reference to the accountant’s report on each supplementary page. But, again, it’s fine to not include a reference to the report.

Preparation of Financial Statement Engagements

Additionally, SSARS provides a nonattest option called the preparation of financial statements (AR-C 70). This option is used by the CPA to issue financial statements that are not subject to the compilation standards. No compilation report is issued. AR-C 70 requires that the accountant either state on each page that “no assurance is provided” or provide a disclaimer that precedes the financial statements. AR-C 70 does not require that the financial statement pages refer to the disclaimer (if provided), but it is permissible to do so. Such a reference might read See Accountant’s Disclaimer.

If your AR-C 70 work product has supplementary information, consider including this same reference (See Accountant’s Disclaimer) on the supplementary pages.

In this post, I tell you how to use the AICPA Consulting Standards (Statement on Standards for Consulting Services). I will also compare AUP engagements with consulting engagement options.

Are you ever asked to perform unusual engagements? Such as a report of a city’s water loss. Or a review of billing and receipts internal controls. Or maybe a test count of widgets in the Macon, Georgia warehouse.

When such requests are made, you might wonder “what professional standards should I follow?” Often the answer is the AICPA Consulting Standards.

AUP or a Consulting Engagement?

Regarding new and unusual engagements, I am sometimes asked, “Should this be an agreed-upon-procedures (AUP) engagement or a consulting engagement?”

My answer: It depends.

Allow me a moment to compare AUPs with Consulting engagements, and then I’ll explain what the decision hinges upon.

Agreed Upon Procedures Engagement

First, consider the AUP option.

AUPs are mainly composed of the following:

Procedures

Findings

You perform the procedures in relation to assertions made by a responsible party.

An example of a procedure and finding follows:

Procedure – Agreed all January 2020 disbursements greater than $20,000 to checks that cleared the bank statement; compared the payee on each check to the payee per the check register.

Finding – All check payees agreed with the exception of check 2394 for $45,000. The payee for this check was I. Cheatum, and the check register reflected a payment to King’s Supply Company.

Additionally, independence is required.

CPA Consulting Engagement

Second, we’ll consider the consulting engagement option.

A consulting engagement is less precise than an AUP and does not necessarily follow the procedures/findings format. There are no specific reporting standards for a consulting engagement, so a CPA can more easily design the engagement to meet various needs. The consulting standards are more flexible than the attestation standards. And this flexibility enables you to be more creative in designing the engagement.

Assertions by a responsible party are not required under the consulting standards.

Moreover, independence is not required.

A consulting report might address the following:

Reading of minutes

Interviews of individual employees

Flowcharting of internal controls

Summary of production statistics

Narrative of business goals and enterprise risks

As you can tell, there are no procedures and findings (though you are not prohibited from doing so). Most CPAs usually perform AUPs when there are specific procedures.

The Best Option

So which is better? An AUP or a consulting engagement?

I’ll say it again: It depends. On what? Third party reliance.

Consider the following:

Will there be external parties (e.g. creditors) placing reliance on the report?

Is the purpose of the report to add credibility to the information (by having the CPA attest to procedures and findings)?

If the answer to either of these questions is yes, then consider the AUP option. Why? The Attestation Standards–the guidance for AUPs–are more defined and rigorous. And AUP procedures tend to be more specific than those in a consulting engagement.

If no third party reliance, then a consulting engagement may be the better option. Always ask, “Who will receive the report?” You need to know who will read and potentially place reliance upon the report. Then design the work product accordingly.

Litigation Exposure

Are consulting engagements riskier than AUPs? Generally, yes. At least, in my opinion.

The safer option is to perform an AUP. In such engagements, you are asked by the client to perform particular procedures. This specificity lowers the risk of potential litigation as it relates to your work product. The flexibility of a consulting engagement, while helpful in designing creative deliverables, can be riskier because of the lack of specific client requirements.

Now, let me provide you with an overview of the Consulting Standards. As you read this primer, consider how flexible the guidance is.

AICPA Consulting Standards Primer

You might call the AICPA Consulting Standards the CPA’s Swiss army knife. Why? Because of the diversity of services you can perform.

What services fall under these standards?

The consulting standards specifically address six areas:

Consultations – e.g., reviewing a business plan

Advisory services – e.g., assistance with strategic planning

Implementation services – e.g., assistance with a merger

Transaction services – e.g., litigation services

Staff and other support services – e.g., controllership services

Product services – e.g., providing packaged training services

CPAs often provide consulting services such as the following:

Consultations with regard to complex transactions

Fraud investigation services

Internal control services

Bankruptcy services

Divorce settlement services

Controllership services

Business plan preparation

Cash management

Software selection

Business disposition planning

Now, let’s review the characteristics of consulting engagements.

Characteristics of a Consulting Engagement

The characteristics of a consulting engagement include the following:

Generally nonrecurring

Requires a CPA with specialized knowledge and skills

More interaction with client

Generally performed for the client (usually, no third party sees the information)

But, what are the workpaper requirements for a consulting engagement?

Consulting Workpaper Requirements

Consulting workpaper requirements are minimal. Nevertheless, documentation is always wise.

The understanding with the client can be oral or in writing (I recommend the latter).

The consulting standards do not require the CPA to prepare workpapers, but you should do so anyway. Theworkpapers are the link between your work and your report. Also, the general standards of the profession, contained in the AICPA Code of Professional Conduct, apply to all services performed by members. The general standards state:

Sufficient Relevant Data. Obtain sufficient relevant data to afford a reasonable basis for conclusions or recommendations in relation to any professional services performed.

By now, you’re probably thinking the Consulting Standards sound easy, I’ll bet the reporting requirements are challenging. Not so, my friend.

Consulting Reports

A report is not required, but if one is provided, the client and CPA determine the content and format. How’s that for flexibility?

No Opinion or Accountant’s Report

For consulting engagements, the CPA does not issue an opinion or any other attestation report.

Subject to Peer Review?

Are deliverables created under the Consulting Standards subject to peer review? No.

The Consulting Standards provide us with a breath of options, enabling you and I to craft services and reports in the manner desired by our clients. This is one Swiss army knife that I will continue to use.