Creating clear financial statement disclosures is not always easy. Creating (unintentional) confusion? Well, that’s another matter.

Clear Financial Statement Disclosures

Let’s pretend that Olympic judges rate your most recent disclosures, flashing scores to a worldwide audience. What do you see? Tens everywhere—or something else?

Balance sheets tend to be clear. Why? The accounting equation. Assets always equal liabilities plus equity. But there is no disclosure equation (darn it), and without such, we flounder in our communication.

CPAs tend to be linear thinkers. We enjoy Pascal more than Hemingway, numbers more than words, debits and credits more than paragraphs. Our brains are wired that way.

But accounting is more than just numbers. It is the communication of financial statements and disclosures. In the name of clear disclosures, I offer these suggestions.

Consider Your Readers

Who will read the financial statements? Owners, lenders, and possibly vendors. Owners—especially those of smaller businesses—may need simpler language. Some CPAs write notes as if CPAs (alone) will read them. While accounting is technical, we need—as much as possible—to simplify.

Use Short Paragraphs

Lengthy paragraphs choke the reader. Breaking long paragraphs into shorter ones makes the print accessible.

Less is more in many instances. When we try to say too much, we sometimes say…too much. Additionally, short sentences are helpful.

Use Short Sentences

CPAs may have invented the run-on sentence. As I read one of those beauties, I feel as though I can’t breathe. And by the end, I’m gasping. Breaking long sentences into shorter ones makes the reader more comfortable. And she will thank you.

Use Shorter Words

CPAs don’t receive merit badges for long, complicated words. Our goal is to communicate, not to impress. For example, split is better than bifurcate.

Attorneys are not our model. I sometimes see notes that are regurgitations of legal agreements, copied word for word—and you can feel the stiltedness. Do your reader a favor and translate the legalese into digestible—and might I say more enjoyable—language.

Use Tables

Long sentences with several numbers can be confusing. Tables are easier to understand.

Write Your Own Note

Too many CPAs copy disclosures from the Internet without understanding the language. Make sure the language is appropriate for your company.

Put Disclosures in the Right Buckets

Think of each disclosure header as a bucket. For example, if the notes include a related party note, then that’s where the related party information goes. If the debt note includes a related party disclosure (and this may be necessary), place a reference in the related party note to the debt disclosure. You don’t want your reader to think all of the related party disclosures are in one place (the related party note) when they are not. The same issue arises with subsequent event notes.

Have a Second Person Review the Notes

When writing, we sometimes think we are clear when we are not. Have a second person review the note for proper punctuation, spelling, structure, and clarity. If you don’t have a second person available, perform a cold review the next day—you will almost always see necessary revisions. I find that reading out loud helps me to assess clarity.

I also use Grammarly to edit documents. The software provides grammar feedback as you write. If you don’t have a second person to review your financials, I recommend it.

Use a Current Disclosure Checklist

Vetting your notes with a disclosure checklist may be the most tedious and necessary step. FASB and GASB continue to issue new statements at a rapid rate, so using a checklist is necessary to ensure completeness.

Winning Gold

I hope these suggestions help you win gold–10s everywhere. I think I hear the national anthem.

Are you ready to implement FASB’s new nonprofit accounting standard? Back in August 2016, FASB issued ASU 2016-14, Presentation of Financial Statements of Not-for-Profit Entities. In this article, I provide an overview of the standard and implementation tips.

New Nonprofit Accounting – Some Key Impacts

What are a few key impacts of the new standard?

Classes of net assets

Net assets released from “with donor restrictions”

Presentation of expenses

Intermediate measure of operations

Liquidity and availability of resources

Cash flow statement presentation

Classes of Net Assets

Presently nonprofits use three net asset classifications:

Unrestricted

Temporarily restricted

Permanently restricted

The new standard replaces the three classes with two:

Net assets with donor restrictions

Net assets without donor restrictions

Terms Defined

These terms are defined as follows:

Net assets with donor restrictions – The part of net assets of a not-for-profit entity that is subject to donor-imposed restrictions (donors include other types of contributors, including makers of certain grants).

Net assets without donor restrictions – The part of net assets of a not-for-profit entity that is not subject to donor-imposed restrictions (donors include other types of contributors, including makers of certain grants).

Presentation and Disclosure

The totals of the two net asset classifications must be presented in the statement of financial position, and the amount of the change in the two classes must be displayed in the statement of activities (along with the change in total net assets). Nonprofits will continue to provide information about the nature and amounts of donor restrictions.

Additionally, the two net asset classes can be further disaggregated. For example, donor-restricted net assets can be broken down into (1) the amount maintained in perpetuity and (2) the amount expected to be spent over time or for a particular purpose.

Net assets without donor restrictions that are designated by the boardfor a specific use should be disclosed either on the face of the financial statements or in a footnote disclosure.

Sample Presentation of Net Assets

Here’s a sample presentation:

Net Assets

Without donor restrictions

Undesignated

$XX

Designated by Board for endowment

XX

XX

With donor restrictions

Perpetual in nature

XX

Purchase of equipment

XX

Time-restricted

XX

XX

Total Net Assets

$XX

Net Assets Released from “With Donor Restrictions”

The nonprofit should disaggregate the net assets released from restrictions:

program restrictions satisfaction

time restrictions satisfaction

satisfaction of equipment acquisition restrictions

appropriation of donor endowment and subsequent satisfaction of any related donor restrictions

satisfaction of board-imposed restriction to fund pension liability

Here’s an example from ASU 2016-14:

Presentation of Expenses

Presently, nonprofits must present expenses by function. So, nonprofits must present the following (either on the face of the statements or in the notes):

Program expenses

Supporting expenses

The new standard requires the presentation of expenses by function and nature (for all nonprofits). Nonprofits must also provide the analysis of these expenses in one location. Potential locations include:

Face of the statement of activities

A separate statement (preceding the notes; not as a supplementary schedule)

Notes to the financial statements

I plan to add a separate statement (like the format below) titled Statement of Functional Expenses. (Nonprofits should consider whether their accounting system can generate expenses by function and by nature. Making this determination now could save you plenty of headaches at the end of the year.)

External and direct internal investment expenses are netted with investment income and should not be included in the expense analysis. Disclosure of the netted expenses is no longer required.

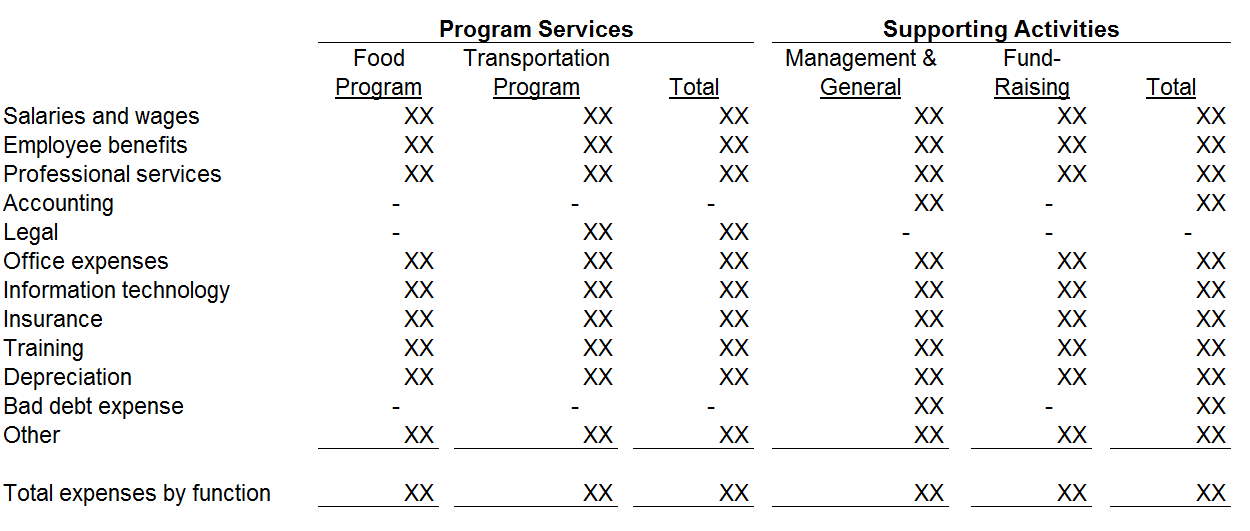

Example of Expense Analysis

Here’s an example of the analysis, reflecting each natural expense classification as a separate row and each functional expense classification as a separate column.

The nonprofit should also disclose how costs are allocated to the functions. For example:

Certain expenses are attributable to more than one program or supporting function. Depreciation is allocated based on a square-footage basis. Salaries, benefits, professional services, office expenses, information technology and insurance, are allocated based on estimates of time and effort.

Intermediate Measure of Operations

If the nonprofit provides a measure of operations on the face of the financial statements and the use of the term “operations” is not apparent, disclose the nature of the reported measure of operations or the items excluded from operations. For example:

Measure of Operations

Learning Disability’s operating revenue in excess of operating expenses includes all operating revenues and expenses that are an integral part of its programs and supporting activities and the assets released from donor restrictions to support operating expenditures. The measure of operations excludes net investment return in excess of amounts made available for operations.

Alternatively, provide the measure of operations on the face of the financial statements by including lines such as operating revenues and operating expenses in the statement of activities. Then the excess of revenues over expenses could be presented as the measure of operations.

Liquidity and Availability of Resources

FASB is shining the light on the nonprofit’s liquidity. Does the nonprofit have sufficient cash to meet its upcoming responsibilities?

Nonprofits should include disclosures regarding the liquidity and availability of resources. The purpose of the disclosures is to communicate whether the organization’s liquid available resources are sufficient to meet the cash needs for general expenditures for one year beyond the balance sheet date. The disclosure should be qualitative (providing information about how the nonprofit manages its liquid resources) and quantitative (communicating the availability of resources to meet the cash needs).

Sample Liquidity and Availability Disclosure

The FASB Codification provides the following example disclosure in 958-210-55-7:

NFP A has $395,000 of financial assets available within 1 year of the balance sheet date to meet cash needs for general expenditure consisting of cash of $75,000, contributions receivable of $20,000, and short-term investments of $300,000. None of the financial assets are subject to donor or other contractual restrictions that make them unavailable for general expenditure within one year of the balance sheet date. The contributions receivable are subject to implied time restrictions but are expected to be collected within one year.

NFP A has a goal to maintain financial assets, which consist of cash and short-term investments, on hand to meet 60 days of normal operating expenses, which are, on average, approximately $275,000. NFP A has a policy to structure its financial assets to be available as its general expenditures, liabilities, and other obligations come due. In addition, as part of its liquidity management, NFP A invests cash in excess of daily requirements in various short-term investments, including certificate of deposits and short-term treasury instruments. As more fully described in Note XX, NFP A also has committed lines of credit in the amount of $20,000, which it could draw upon in the event of an unanticipated liquidity need.

Alternatively, the nonprofit could present tables (see 958-210-55-8) to communicate the resources available to meet cash needs for general expenditures within one year of the balance sheet date.

Cash Flow Statement Presentation

A nonprofit can use the direct or indirect method to present its cash flow information. The reconciliation of changes in net assets to cash provided by (used in) operating activities is not required if the direct method is used.

Consider whether you want to incorporate additional changes that will be required by ASU 2016-18, Statement of Cash Flows–Restricted Cash. If your nonprofit has no restricted cash, then this standard is not applicable.

You can early implement ASU 2016-18. (The effective date is for fiscal years beginning after December 15, 2018.) Once this standard is effective, you’ll include restricted cash in your definition of cash. The last line of the cash flow statement might read as follows: Cash, Cash Equivalents, and Restricted Cash.

Effective Date of ASU 2016-14

The effective date for 2016-14, Not-for-Profit Entities, is for fiscal periods beginning after December 15, 2017 (2018 calendar year-ends and 2019 fiscal year-ends). The standard can be early adopted.

For comparative statements, apply the standard retrospectively.

If presenting comparative financial statements, the standard does allow the nonprofit to omit the following information for any periods presented before the period of adoption:

Analysis of expenses by both natural classification and functional classification (the separate presentation of expenses by functional classification and expenses by natural classification is still required). Nonprofits that previously were required to present a statement of functional expenses do not have the option to omit this analysis; however, they may present the comparative period information in any of the formats permitted in ASU 2014-16, consistent with the presentation in the period of adoption.

Disclosures related to liquidity and availability of resources.

The Accounting and Review Services Committee (ARSC) issued SSARS 22Compilation of Pro Forma Financial Information. You may remember that ARSC did not address pro forma information in SSARS 21. SSARS 22 clarifies AR 120 Compilation of Pro Forma Information and codifies it as AR-C 120.

Pro Forma Information

So what is pro forma information? It is a presentation that shows what the significant effects on historical financial information might have been had a consummated or proposed transaction (or event) occurred at an earlier date.

To understand SSARS 22, let’s answer a few questions.

Examples of Pro Forma Information

Examples of pro forma information include presenting financial statements for the following:

Business combinations

The selling of a significant part of a business

A change in the capitalization of an entity

Again we are providing financial information as though the transaction or event has–already–occurred.

Required Disclosures

In pro forma financial information, what should be disclosed?

A description of the transaction (or event) that is reflected in the presentation

The date on which the transaction (or event) is assumed to occur

The financial reporting framework

The source of the financial information

The significant assumptions used

Any significant uncertainties about those assumptions

A statement that the pro forma information should be read in conjunction with the related historical information and that the pro forma information is not necessarily indicative of the results that would have been attained had the transaction (or event) actually taken place

Independence

Must the accountant consider his or her independence? Yes, since this is a compilation engagement. (Note: The preparation of the pro forma information is considered a nonattest service.)

Acceptance and Continuance

Should the accountant perform acceptance and continuance procedures? Yes.

Engagement Letter

Is an engagement letter required? Yes, and it must be signed by the accountant’s firm and management or those charged with governance.

Compilation Procedures

What compilation procedures should be performed?

Read the pro forma financial information to determine if it is appropriate in form and free from obvious material misstatement

Obtain an understanding of the underlying transaction or event (that the pro forma information is based upon)

Determine that management includes:

Complete financial statementsfor the most recent year (or from the preceding year if financial statements for the most recent year are not yet available) or make such financial statements readily available (e.g., post on a public website)

If pro forma financial information is presented for an interim period, either historical interim financial information for that period (which may be in condensed form) or make such interim information readily available

For business combinations, the relevant financial information for the significant parts of the combined entity

Determine that the information in the preceding bullet has been subjected to a compilation, review or an audit

Determine that the compilation, review or audit report on the historical information is included in any document containing the pro forma financial information (or made readily available such as on a public website)

Determine whether the significant assumptions and uncertainties are disclosed

Determine whether the source of the historical financial information on which the pro forma information is based is appropriately identified

Pro Forma in Conjunction with Other Services

Can the pro forma engagement be performed in conjunction with a compilation, review or an audit? Yes. Alternatively, the pro forma engagement can be performed separately.

Required Documentation

What documentation is to be retained in the file?

Engagement letter

The results of procedures performed

Copy of the pro forma financial information

Copy of the accountant’s compilation report

Compilation Report Required

Is a compilation report to be issued? Yes. (See sample report below.)

Is the accountant offering any assurance regarding the pro forma information? No.

Can the pro forma compilation report be added to the accountant’s report on historical financial statements? Yes. Alternatively, the pro forma compilation report can be presented separately.

Effective Date of SSARS 22

What’s the effective date of SSARS 22? The standard is effective for compilation reports on pro forma financial information dated on or after May 1, 2017.

Potential New Service for Your Clients

If you are not already providing pro forma information to clients, consider suggesting this service when appropriate. Clients may find pro forma information helpful in evaluating the potential sale of stock, the borrowing of funds for a project, or the sale of a part of the business.

Sample SSARS 22 Compilation Report

Exhibit B of SSARS 22 provides the following sample compilation report on pro forma financial information:

Management is responsible for the accompanying pro forma condensed balance sheet of XYZ Company as of December 31, 20X1, and the related pro forma condensed statement of income for the year then ended (pro forma financial information), based on the criteria in Note 1. The historical condensed financial statements are derived from the financial statements of XYZ Company, on which I (we) performed a compilation engagement, and of ABC Company, on which other accountants performed a compilation engagement. The pro forma adjustments are based on management’s assumptions described in Note 1. (We) have performed a compilation engagement in accordance with Statements on Standards for Accounting and Review Services promulgated by the Accounting and Review Services Committee of the AICPA. I (we) did not examine or review the pro forma financial information nor was (were) I (we) required to perform any procedures to verify the accuracy or completeness of the information provided by management. Accordingly, I (we) do not express an opinion, a conclusion, nor provide any form of assurance on the pro forma financial information.

The objective of this pro forma financial information is to show what the significant effects on the historical financial information might have been had the underlying transaction (or event) occurred at an earlier date. However, the pro forma condensed financial statements are not necessarily indicative of the results of operations or related effects on financial position that would have been attained had the above mentioned transaction (or event) actually occurred at such earlier date.

[Additional paragraph(s) may be added to emphasize certain matters relating to the compilation engagement or the subject matter.]

[Signature of accounting firm or accountant, as appropriate] [Accountant’s city and state] [Date of the accountant’s report]