Independence in Attest Engagements

By Charles Hall | Auditing , Preparation, Compilation & Review

Independence in attest engagements in critical.

Peer reviewers continue to focus on independence documentation. Today I’ll provide you with examples of what peer reviewers are looking for and guidance to keep you out of hot water.

Documentation of Nonattest Services

Peer reviews focus upon nonattest services provided to attest clients. How do we know? Well, see the peer review checklist question below (for an attest engagement).

The big “no-no” is to assume management responsibilities and then perform an attest service. Why? Performing management responsibilities impairs your independence.

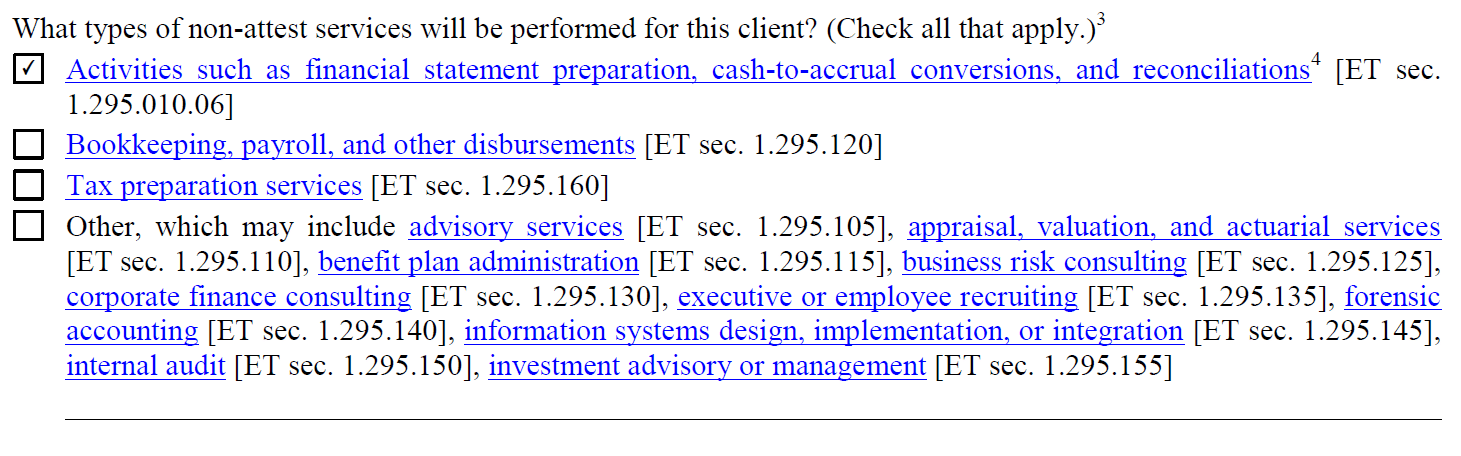

Preparing Financial Statements

Below is another question from the peer review checklists. Notice the first item below: Accepting responsibility for the preparation and fair presentation of the client’s financial statements. The client (not the auditor) must assume responsibility for the financial statements.

If the client can’t–or is unwilling to–assume responsibility for the financial statements, then we are not independent, and we cannot perform an audit or a review. This assumption of responsibility does not mean the client has the ability to create financial statements, but it does mean that:

- that the client will oversee the nonattest service,

- the client will evaluate the adequacy and results of the nonattest service, and

- the client will accept responsibility for the nonattest service

If we prepare financial statements and perform an audit, review, or compilation, we have performed a nonattest service and an attest service. Why is this important? Because if we perform a nonattest service and an attest service for the same client, we must assess our independence. And if we are not independent, then we can’t perform an audit or review engagement. (It is permissible to perform the compilation engagement when independence is impaired, but the accountant must say–in the compilation report–that he is not independent.)

Other Peer Review Questions

The peer review checklists also ask for:

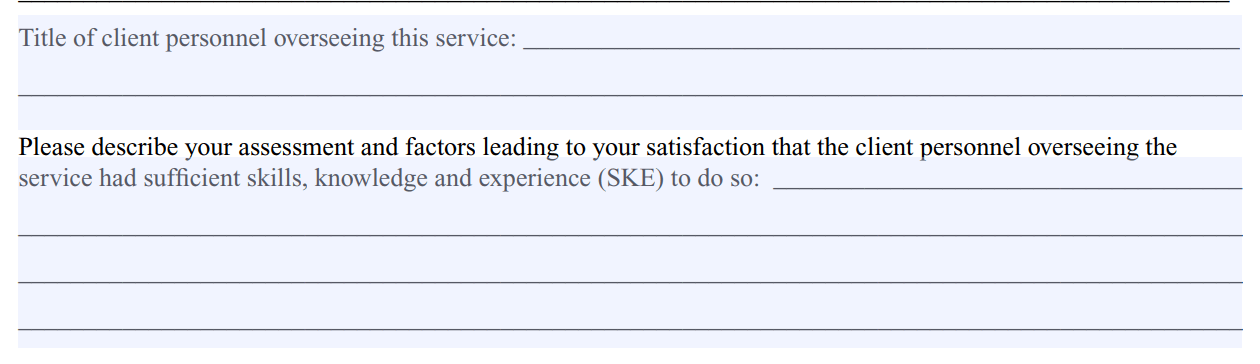

- The name and title of the client personnel overseeing the nonattest service and

- A description of the accountant’s “assessment and factors leading to your satisfaction that the client personnel overseeing the service had sufficient skills, knowledge and experience.”

Separate Form to Document Independence

So do we need a separate form in our file to document independence?

It certainly would not hurt, and I suggest that you do. PPC and CCH offer such forms (and I am sure other work paper providers do the same). These forms provide a place to document all nonattest services and to assess and document our client’s ability to assume responsibility for the nonattest services.

The PPC and CCH forms also address the cumulative effect of performing multiple nonattest services. The AICPA has stated that the performance of multiple nonattest services can impair independence. So you should document your consideration of whether the cumulative nonattest services create a problem. Peer review checklists ask if we documented this consideration.

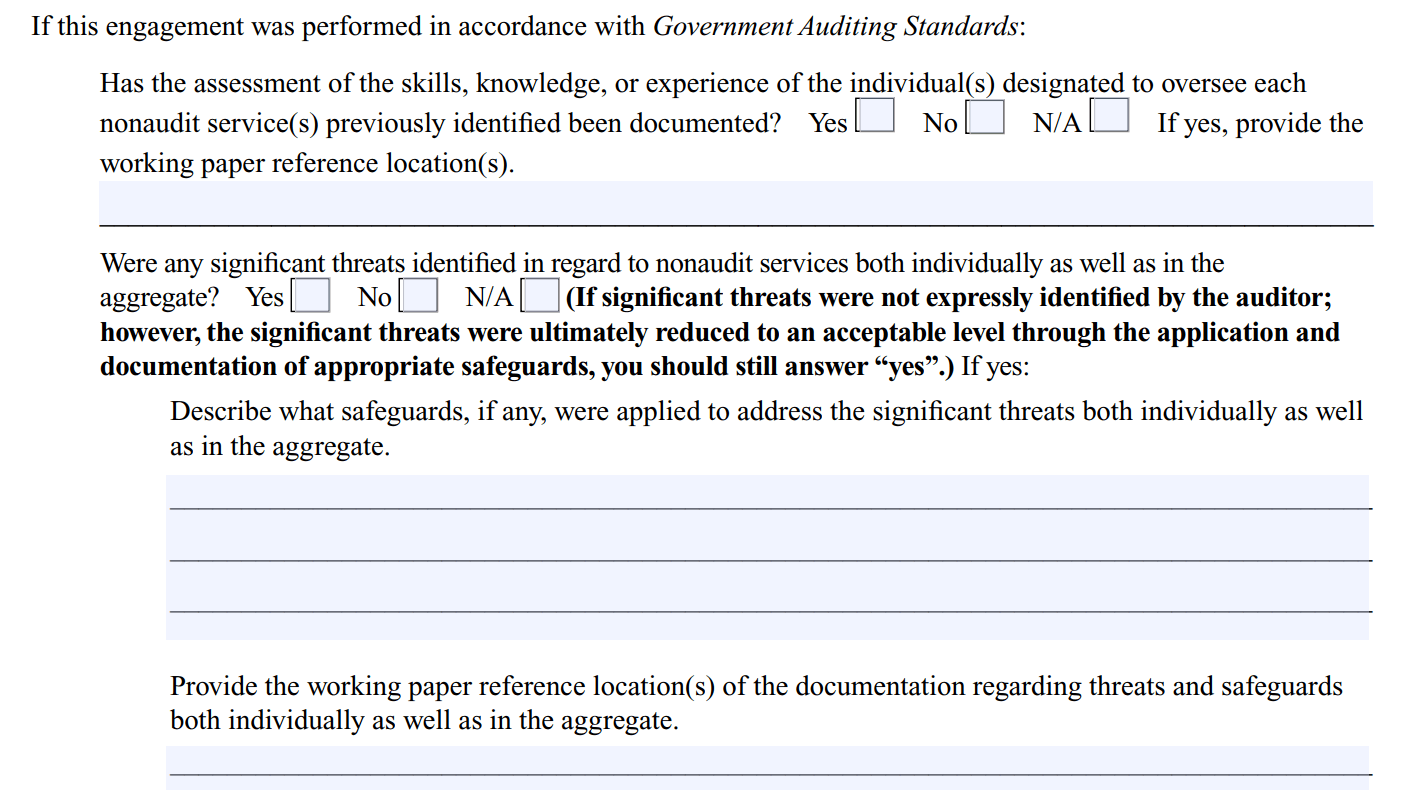

Additionally, if significant threats are present, the accountant should document the safeguard(s) used to mitigate the risk. This documentation is particularly crucial in Yellow Book engagements. The PPC and CCH independence forms will assist you with this documentation. Below are peer review checklist questions:

Alignment in Independence Documentation

We should–in the engagement letter–specify the nonattest services and the responsibilities of management. If you are performing an audit or a review engagement, add additional language to the representation letter regarding the nonattest services performed and the client’s responsibility for those services.

So I am suggesting you document the nonattest services in three places:

- Engagement letter,

- Independence form, and

- Representation letter (when relevant)

And when you do, please make sure the nonattest services listed in each document are the same.

Nonattest Services and Independence

Here’s a video that explains nonattest services and how to document your independence in regard to them.