Knowing how to perform compilation engagements is important for CPAs. Below I provide an overview of the salient points of AR-C 80, Compilation Engagements. I also provide a sample accountant’s compilation report.

Compilation Guidance

The guidance for compilations is located in AR-C 80, Compilation Engagements.

Applicability of AR-C 80

The accountant should perform a compilation engagement when he is engaged to do so.

A compilation engagement letter should be prepared and signed by the accountant or the accountant’s firm and management or those charged with governance. An engagement letter to only prepare financial statements is not a trigger for the performance of a compilation engagement.

Previously (in the SSARS 19 days), the preparation and submission of financial statements to a client triggered the performance of a compilation engagement. Now, compilation engagement guidance is applicable only when the accountant is engaged to (requested to) perform a compilation.

Objectives

The objectives of the accountant in a compilation engagement are to:

Assist management in the presentation of financial statements

Report on the financial statements in accordance with the compilation engagement section of the SSARSs

Do you ever want to include justone disclosure in your financial statements without providing all the notes? Selected disclosures can be included in certain situations, including when you omit substantially all disclosures.

Do professional standards allow this? Yes. But only if you use AR-C 70 (the preparation guidance) or AR-C 80 (the compilation guidance).

Made with Canva

Selected Disclosures in Compilations

As you probably already know, a CPA can issue compiled financial statements without disclosures as long as the compilation report discloses the omission. An example follows.

Management has elected to omit substantially all of the disclosures required by accounting principles generally accepted in the United States of America. If the omitted disclosures were included in the financial statements, they might influence the user’s conclusions about the Company’s financial position, results of operations and cash flows. Accordingly, the financial statements are not designed for those who are not informed about such matters.

If the financial statements include one or two notes, then the financial statements still omit substantially all of the disclosures, so the accountant (still) uses the wording in the preceding paragraph.

Sample Selected Disclosure

An example of a selected disclosure follows:

ABC Company

Selected Information –

Substantially All Disclosures Required by Accounting Principles

Generally Accepted in the United States of America are Not Included

December 31, 2020

Note 1. Long-Term Debt.

ABC Company borrowed $450,000 on July 15, 2020, from XYZ Bank. The rate of interest is 5%, and the loan is collateralized by equipment of the Company. Payments are $10,000 per month plus interest for two years with a balloon payment for the balance of the amount owed.

Additionally, you can omit substantially all disclosures in a preparation engagement.

Preparation Engagements

AR-C 70 says:

The accountant may prepare financial statements that include disclosures about only a few matters in the notes to the financial statements. Such disclosures may be labeled “Selected Information—Substantially All Disclosures Required by [the applicable financial reporting framework] Are Not Included.”

So, the selected-disclosure option is available in a Preparation of Financial Statements engagement. Include the required disclaimer at the bottom of the page such as “No assurance is provided on these financial statements.”

Other Considerations

The accountant should consider whether management’s election to include only selected disclosures causes the financial statements to be misleading (for example, by omitting the disclosures that contain negative information). If so, the accountant should request that the financial statements be revised to include the omitted disclosures.

The selected-disclosure option is not available for financial statements subject to a review engagement. Such financial statements must be full disclosure.

What About You?

Do you ever use this selected-disclosure option? Any reservations about doing so?

What financial statement references are required at the bottom of financial statement pages? Is there a difference in the references in audited statements and those in compilations or reviews? What wording should be placed at the bottom of supplementary pages? Below I answer these questions.

Audited Financial Statements and Supplementary Information

First, let’s look at financial statement references in audit reports.

While generally accepted accounting principles do not require financial page references to the notes, it is a common practice to do so. Here are examples:

See notes to the financial statements.

The accompanying notes are an integral part of these financial statements.

See accompanying notes.

Accountants can also–though not required–reference specific disclosures on a financial statement page. For example, See Note 6 (next to the Inventory line on a balance sheet). It is my preference to use general references such as See accompanying notes.

Audit standards do not require financial statement page references to the audit opinion.

Supplementary pages should not include a reference to the notes or the opinion.

The Statements on Standards for Accounting and Review Services (SSARS) do not require a reference (on financial statement pages) to the compilation or review report; however, it is permissible to do so. What do I do? I do not refer to the accountant’s report. I include See accompanying notes at the bottom of each financial statement page (when notes are included). This reference to notes, however, is not required, even when notes are included. (Notes can be omitted in compilation engagements.)

You are not required to include a reference to the accountant’s report on the supplementary information pages. Examples include:

See Accountant’s Compilation Report.

See Independent Accountant’s Review Report.

What do I do? I include a reference to the accountant’s report on each supplementary page. But, again, it’s fine to not include a reference to the report.

Preparation of Financial Statement Engagements

Additionally, SSARS provides a nonattest option called the preparation of financial statements (AR-C 70). This option is used by the CPA to issue financial statements that are not subject to the compilation standards. No compilation report is issued. AR-C 70 requires that the accountant either state on each page that “no assurance is provided” or provide a disclaimer that precedes the financial statements. AR-C 70 does not require that the financial statement pages refer to the disclaimer (if provided), but it is permissible to do so. Such a reference might read See Accountant’s Disclaimer.

If your AR-C 70 work product has supplementary information, consider including this same reference (See Accountant’s Disclaimer) on the supplementary pages.

Peer reviewers continue to focus on independence documentation. Today I’ll provide you with examples of what peer reviewers are looking for and guidance to keep you out of hot water.

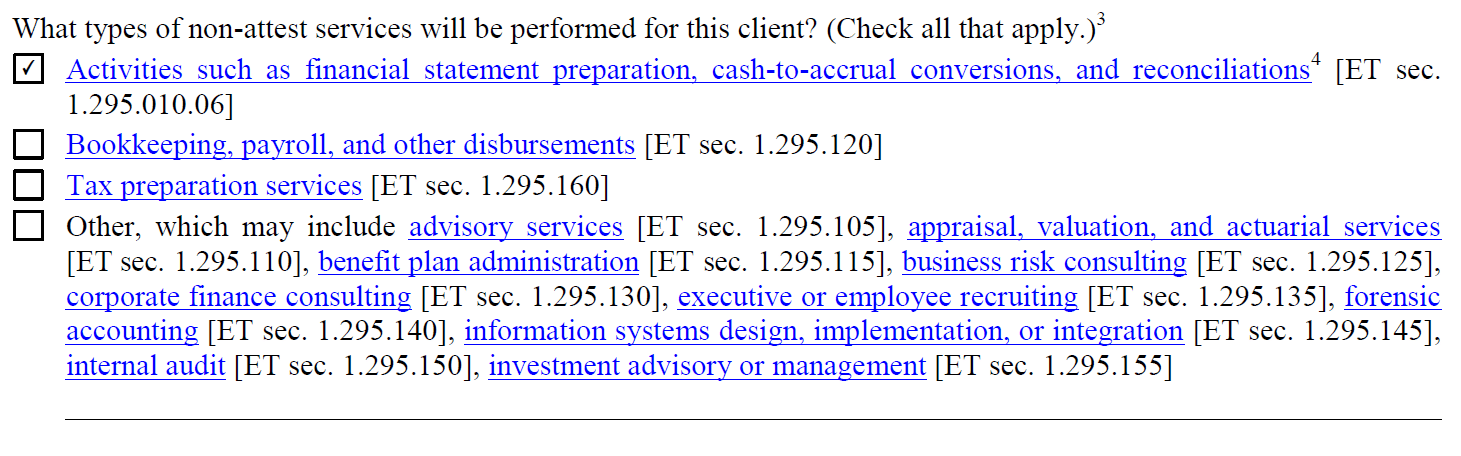

Documentation of Nonattest Services

Peer reviews focus upon nonattest services provided to attest clients. How do we know? Well, see the peer review checklist question below (for an attest engagement).

The big “no-no” is to assume management responsibilities and then perform an attest service. Why? Performing management responsibilities impairs your independence.

Preparing Financial Statements

Below is another question from the peer review checklists. Notice the first item below: Accepting responsibility for the preparation and fair presentation of the client’s financial statements. The client (not the auditor) must assume responsibility for the financial statements.

If the client can’t–or is unwilling to–assume responsibility for the financial statements, then we are not independent, and we cannot perform an audit or a review. This assumption of responsibility does not mean the client has the ability to create financial statements, but it does mean that:

that the client will oversee the nonattest service,

the client will evaluate the adequacy and results of the nonattest service, and

the client will accept responsibility for the nonattest service

If we prepare financial statements and perform an audit, review, or compilation, we have performed a nonattest service and an attest service. Why is this important? Because if we perform a nonattest service and an attest service for the same client, we must assess our independence. And if we are not independent, then we can’t perform an audit or review engagement. (It is permissible to perform the compilation engagement when independence is impaired, but the accountant must say–in the compilation report–that he is not independent.)

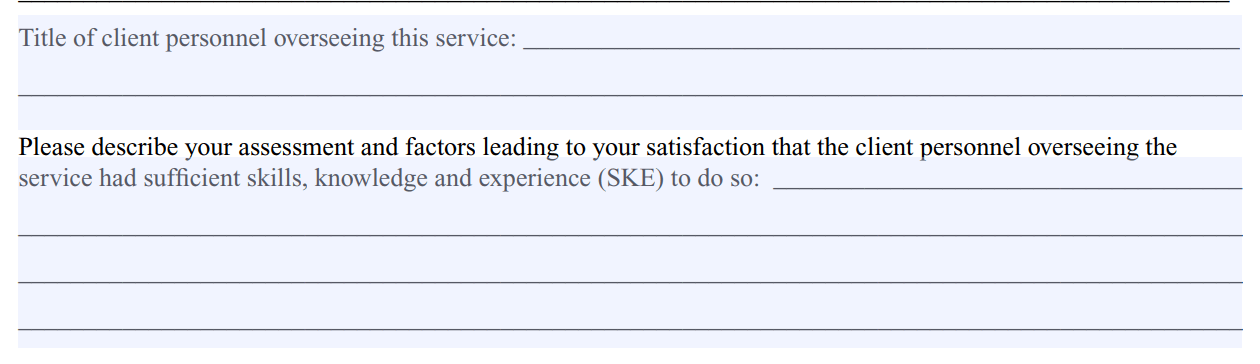

Other Peer Review Questions

The peer review checklists also ask for:

The name and title of the client personnel overseeing the nonattest service and

A description of the accountant’s “assessment and factors leading to your satisfaction that the client personnel overseeing the service had sufficient skills, knowledge and experience.”

Separate Form to Document Independence

So do we need a separate form in our file to document independence?

It certainly would not hurt, and I suggest that you do. PPC and CCH offer such forms (and I am sure other work paper providers do the same). These forms provide a place to document all nonattest services and to assess and document our client’s ability to assume responsibility for the nonattest services.

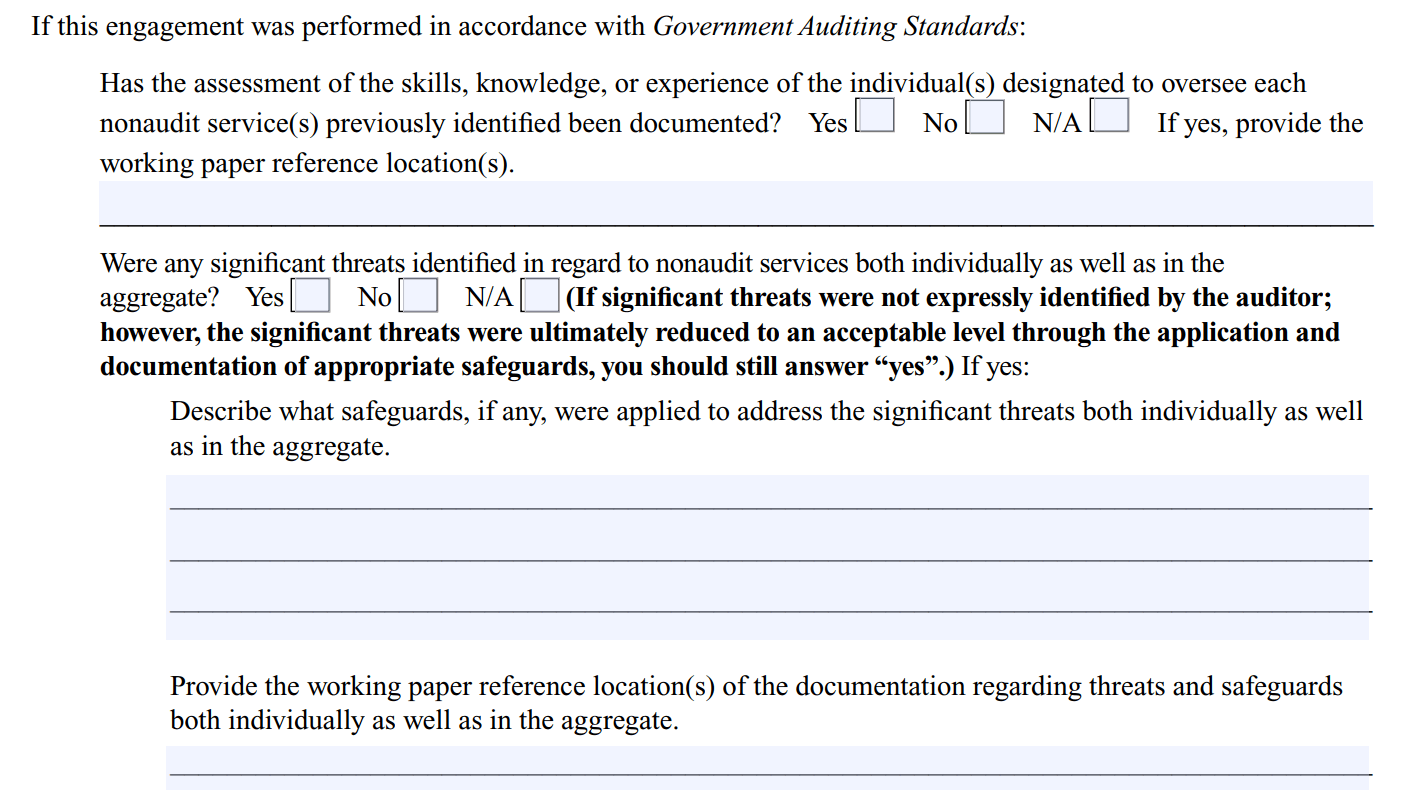

The PPC and CCH forms also address the cumulative effect of performing multiple nonattest services. The AICPA has stated that the performance of multiple nonattest services can impair independence. So you should document your consideration of whether the cumulative nonattest services create a problem. Peer review checklists ask if we documented this consideration.

Additionally, if significant threats are present, the accountant should document the safeguard(s) used to mitigate the risk. This documentation is particularly crucial in Yellow Book engagements. The PPC and CCH independence forms will assist you with this documentation. Below are peer review checklist questions:

Alignment in Independence Documentation

We should–in the engagement letter–specify the nonattest services and the responsibilities of management. If you are performing an audit or a review engagement, add additional language to the representation letter regarding the nonattest services performed and the client’s responsibility for those services.

So I am suggesting you document the nonattest services in three places:

Engagement letter,

Independence form, and

Representation letter (when relevant)

And when you do, please make sure the nonattest services listed in each document are the same.

Nonattest Services and Independence

Here’s a video that explains nonattest services and how to document your independence in regard to them.

Do you need to concern yourself with going concern in compilation and review engagements? Yes, if the financial statements are prepared in accordance with the FASB Codification. But is going concern relevant to special purpose frameworks such as the cash basis or tax basis financial statements. Yes, going concern is in play even with special purpose frameworks. This post provides an overview of what you need to know about going concern as it relates to compilation and review engagements.

A while back I wrote a post about ASU 2014-15, Disclosure of Uncertainties about an Entity’s Ability to Continue as a Going Concern, which was effective for years ending after December 15, 2016. This standard requires companies to include certain disclosures when substantial doubt is present. So, we know that financial statements prepared in accordance with GAAP must include these disclosures. Otherwise, there is a GAAP departure. And in an audit, we modify our opinion when there is a departure.

Going Concern in Compilation Engagements

But what about financial statements subject to a compilation engagement, especially when substantially all disclosures are omitted? Is it permissible for the CPA to ignore the going concern standard since it just requires disclosures? Yes, but be careful. Ask yourself whether the financial statements would be misleading (without the going concern disclosure). If they are misleading, then include a selected disclosure regarding going concern. Also, consider adding an emphasis-of-matter paragraph (regarding going concern) to your compilation report.

Consider the following scenario. Your client (who has significant going concern issues) takes your compilation report (which has no emphasis of a matter paragraph) and their financial statements (that has no disclosures) to a local bank. It’s obvious that the company is not doing well. But the bank makes a large loan anyway, and later, the company defaults on the loan. Then the bank files suit against you (the CPA) asserting that you issued the compilation report without the emphasis-of-matter paragraph and that you knew the financial statements had no going concern disclosure. The bank says the financial statements were misleading.

While the emphasis-of-matter paragraph is not required, consider adding one anyway.

Going Concern in Review Engagements

Since review engagements require full disclosure, going concern disclosures are not optional when substantial doubt exists in GAAP financial statements. They must be provided. If they are not, a GAAP departure exists.

So what going concern procedures should you perform in a review engagement?

In regard to going concern when the financial reporting framework includes going concern requirements (e.g. GAAP), AR-C 90.65 states:

If the applicable financial reporting framework includes requirements for management to evaluate the entity’s ability to continue as a goingconcern for a reasonable period of time in preparing financial statements, the accountant should perform review procedures related to the following:

Whether the going concern basis of accounting is appropriate

Management’s evaluation of whether there are conditions or events that raised substantial doubt about the entity’s ability to continue as a going concern

If there are conditions or events that raised substantial doubt about the entity’s ability to continue as a goingconcern, management’s plans to mitigate those matters

The adequacy of the related disclosures in the financial statements

In regard to going concern when the applicable financial reporting framework does not address going concern (e.g., tax basis), AR-C 90.66 states:

If the applicable financial reporting framework does not include a requirement for management to evaluate the entity’s ability to continue as a going concern for a reasonable period of time in preparing financial statements and conditions or events that raise substantial doubt about an entity’s ability to continue as a going concern for a reasonable period of time existed at the date of the prior period financial statements (regardless of whether the substantial doubt was alleviated by the accountant’s consideration of management’s plans) or, in the course of performing review procedures on the current period financial statements, the accountant becomes aware of conditions or events that raise substantial doubt about the entity’s ability to continue as a going concern, the accountant should do the following:

Inquire of management whether the going concern basis of accounting is appropriate.

Inquire of management about its plans for dealing with the adverse effects of the conditions and events.

Consider the adequacy of the disclosure about such matters in the financial statements.

SSARS 24 does say that the nature and extent of procedures performed regarding going concern are a matter of professional judgment. If the audited entity has a history of profitable operations and access to financing, inquiry alone might be sufficient in a review engagement.

Going Concern Paragraph in a Review Report

If the accountant concludes that substantial doubt will remain for a reasonable period of time, an emphasis-of-matter paragraph is required in the review report. (Some reporting frameworks specify a “reasonable period of time.” For GAAP, it is one year from the date the financial statements are issued or are available to be issued.)

AR-C 90.A123 provides the following example of a going concern paragraph in a review engagement when (1) substantial doubt exists for a reasonable period of time, (2) management’s plans don’t alleviate the substantial doubt, and (3) the reporting framework requires a note disclosure.

Emphasis of Matter

The accompanying financial statements have been prepared assuming that the Company will continue as a going concern. As discussed in Note X to the financial statements, the Company has suffered recurring losses from operations, has a net capital deficiency, and has stated that substantial doubt exists about the Company’s ability to continue as a going concern. Management’s evaluation of the events and conditions and management’s plans regarding these matters are also described in Note X. The financial statements do not include any adjustments that might result from the outcome of this uncertainty. Our conclusion is not modified with respect to this matter.

Representation Letter in Review Engagements

Be sure to update your representation letter when performing review engagements. SSARS 24 tweaked some language in the letter and added additional wording such as the following:

Management has disclosed to the accountant all information relevant to use of the going concern assumption in the financial statements.

Special Purpose Frameworks and Going Concern

While the cash, modified cash, or tax bases of accounting do not address going concern, accountants still need to consider the effects of negative financial conditions and trends. Why? When using a special purpose framework (like the tax basis), the accountant should follow the guidance in GAAP. No, that doesn’t mean your disclosures are just like GAAP, but it does mean they are similar to GAAP.

Since GAAP tells the financial statement preparer to consider whether substantial doubt exists, then persons creating cash basis, modified cash basis or tax basis financial statements should do the same. If substantial doubt is present, going concern disclosures are necessary.

So, what is substantial doubt? The FASB Codification defines it this way:

Substantial doubt about the entity’s ability to continue as a going concern is considered to exist when aggregate conditions and events indicate that it is probable that the entity will be unable to meet obligations when due within one year of the date that the financial statements are issued or are available to be issued.

If substantial doubt is present and going concern disclosures are not included in full disclosure compilations or reviews, then modify your accountant’s report (for the departure).