SSARS 21: What Have We Learned?

By Charles Hall | Preparation, Compilation & Review

SSARS 21 has been in existence since October 2014. What have we learned about this standard?

(SSARS 22 and SSARS 23 were subsequently added, but most of the SSARS 21 guidance remains as originally issued.)

Preparation of Financial Statements or Compilation Reports

Before SSARS 21, if an accountant created financial statements and submitted them to a client, he had to issue a compilation report. Now, using the Preparation of Financial Statements part of SSARS 21 (AR-C 70), an accountant can create and provide financial statements without a compilation report. Such financial statements can be provided to third parties such as banks–again with no compilation report. So, how have accountants responded to the option to provide financial statements to clients without a compilation report?

It has been my observation that many accountants continue to perform compilation engagements (rather than use the preparation option). Why? I think we are creatures of habit. We have issued compilation reports for so long that we’re comfortable doing so–and we continue to do the same. Also, as we’ll see in a minute, performing a compilation doesn’t take much additional time.

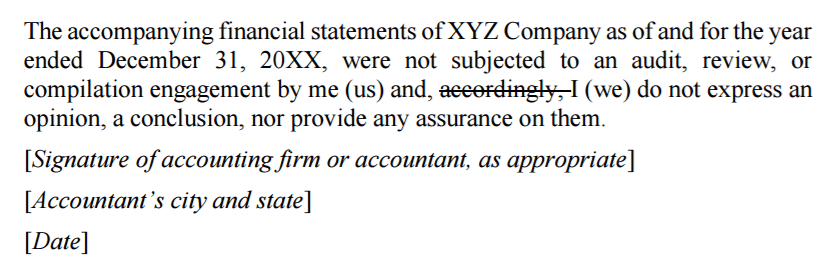

Some accountants, however, are using AR-C 70. They are issuing financial statements without a compilation report and stating that “no assurance is provided” on each page–or, as the standard allows, placing a disclaimer page in front of the financial statements.

Who Should Use the Preparation Standard?

So, who uses AR-C 70? Accountants with limited time.

Suppose, for example, that a client wants a balance sheet and nothing else. You can create the balance sheet in Excel and put “no assurance is provided” at the bottom of the page. And you’re done–with the exception of obtaining a signed engagement letter. (Accountants should document any significant consultations or professional judgments, but usually, there are none.)

Can I Avoid the Engagement Letter?

You may be thinking, “Charles, I’m not sure I’m saving much time if I have to create an engagement letter. Getting a signed engagement letter might even take more time than preparing the balance sheet.” Yes, that is true. So, is there a situation where the engagement letter is not required? Yes, sometimes.

Financial Statements as a Byproduct

You can provide the balance sheet to a client without obtaining an engagement letter if the statement preparation is a byproduct of another service (as long as you have not been engaged to prepare the financial statement). For example, if you’re preparing a tax return and create the balance sheet as a byproduct of the tax service, you are not required to obtain a SSARS engagement letter? Why? Because you have not been engaged to prepare the financial statement. The trigger for AR-C 70 is whether you have been engaged to prepare financial statements.

QuickBooks Bookkeeping

The same is true if you provide bookkeeping services using QuickBooks in the Cloud. If you have not been engaged to prepare financial statements and the online software allows you to print the financial statements, you are not in the soup. That is, you are not following AR-C 70–because you have not been engaged to prepare financial statements. If your client asks you to perform bookkeeping service in a cloud-based accounting package (such as QuickBooks) and to prepare financial statements, you are engaged. Then you must follow AR-C 70 and obtain an engagement letter–and follow the other requirements of the standard.

Regardless, we need to be clear about the intended service.

Compilation Engagements

In most compilations, the accountant prepares the financial statements and performs the compilation engagement. Notice these are two different services: (1) preparing the financial statements and (2) performing the compilation. It is possible for your client to create the financial statement and for you (the accountant) to perform the compilation, though this is rare. If you do both, the preparation of financial statements is not performed using AR-C 70. So what standard should you follow for the preparation of the financial statements. There is none. You are just performing a nonattest service. Then you’ll perform the compilation engagement using AR-C 80.

So, the question at this point is whether you should prepare financial statements using AR-C 70 or create the financial statements and perform a compilation using AR-C 80. (Technically, the choice is the clients, but you are explaining the differences to them.)

Additional Time for Compilations

How much extra time does it take to perform a compilation engagement after the financial statements are created? Not much. You are only placing a compilation report on your letterhead (rather than stating that “no assurance is provided” on each page or providing a disclaimer that precedes the financial statements).

What other procedures are required for a compilation (versus providing the financial statements under AR-C 70)? You are reading the financial statements to see if they are appropriate. And since you just created the statements, that shouldn’t take much time.

Regardless, both AR-C 70 and AR-C 80 require signed engagement letters. So if you’ve been engaged to prepare financial statements or perform a compilation, there is no getting around the requirement for an engagement letter.

Is a Preparation or a Compilation Service Best?

So which is better? Using AR-C 70 (Preparation of Financial Statements) or AR-C 80 (Compilation Engagements)? It depends.

Some banks desire a compilation report, so in that case, of course, you are going to–at the request of the client–perform a compilation engagement.

Also, some CPAs feel safer issuing a compilation report that spells out (in greater detail than a preparation disclaimer) what is done and what is not done. We don’t know yet whether a preparation service creates greater legal exposure than a compilation. But we will with time. After a few years of using SSARS 21, I think our insurance companies will tell us whether one service creates more exposure than another. So far, I have not seen any such studies. Why? SSARS 21 has been in use only a couple of years.

Another factor to consider is peer review. The AICPA standards do not require a peer review if you only provide financial statements using AR-C 70. But check with your state board of accountancy; some states require peer review, regardless.

For the most efficient way to issue financial statements, click here.