What financial statement references are required at the bottom of financial statement pages? Is there a difference in the references in audited statements and those in compilations or reviews? What wording should be placed at the bottom of supplementary pages? Below I answer these questions.

Audited Financial Statements and Supplementary Information

First, let’s look at financial statement references in audit reports.

While generally accepted accounting principles do not require financial page references to the notes, it is a common practice to do so. Here are examples:

See notes to the financial statements.

The accompanying notes are an integral part of these financial statements.

See accompanying notes.

Accountants can also–though not required–reference specific disclosures on a financial statement page. For example, See Note 6 (next to the Inventory line on a balance sheet). It is my preference to use general references such as See accompanying notes.

Audit standards do not require financial statement page references to the audit opinion.

Supplementary pages should not include a reference to the notes or the opinion.

The Statements on Standards for Accounting and Review Services (SSARS) do not require a reference (on financial statement pages) to the compilation or review report; however, it is permissible to do so. What do I do? I do not refer to the accountant’s report. I include See accompanying notes at the bottom of each financial statement page (when notes are included). This reference to notes, however, is not required, even when notes are included. (Notes can be omitted in compilation engagements.)

You are not required to include a reference to the accountant’s report on the supplementary information pages. Examples include:

See Accountant’s Compilation Report.

See Independent Accountant’s Review Report.

What do I do? I include a reference to the accountant’s report on each supplementary page. But, again, it’s fine to not include a reference to the report.

Preparation of Financial Statement Engagements

Additionally, SSARS provides a nonattest option called the preparation of financial statements (AR-C 70). This option is used by the CPA to issue financial statements that are not subject to the compilation standards. No compilation report is issued. AR-C 70 requires that the accountant either state on each page that “no assurance is provided” or provide a disclaimer that precedes the financial statements. AR-C 70 does not require that the financial statement pages refer to the disclaimer (if provided), but it is permissible to do so. Such a reference might read See Accountant’s Disclaimer.

If your AR-C 70 work product has supplementary information, consider including this same reference (See Accountant’s Disclaimer) on the supplementary pages.

Are you ready to implement FASB’s new nonprofit accounting standard? Back in August 2016, FASB issued ASU 2016-14, Presentation of Financial Statements of Not-for-Profit Entities. In this article, I provide an overview of the standard and implementation tips.

New Nonprofit Accounting – Some Key Impacts

What are a few key impacts of the new standard?

Classes of net assets

Net assets released from “with donor restrictions”

Presentation of expenses

Intermediate measure of operations

Liquidity and availability of resources

Cash flow statement presentation

Classes of Net Assets

Presently nonprofits use three net asset classifications:

Unrestricted

Temporarily restricted

Permanently restricted

The new standard replaces the three classes with two:

Net assets with donor restrictions

Net assets without donor restrictions

Terms Defined

These terms are defined as follows:

Net assets with donor restrictions – The part of net assets of a not-for-profit entity that is subject to donor-imposed restrictions (donors include other types of contributors, including makers of certain grants).

Net assets without donor restrictions – The part of net assets of a not-for-profit entity that is not subject to donor-imposed restrictions (donors include other types of contributors, including makers of certain grants).

Presentation and Disclosure

The totals of the two net asset classifications must be presented in the statement of financial position, and the amount of the change in the two classes must be displayed in the statement of activities (along with the change in total net assets). Nonprofits will continue to provide information about the nature and amounts of donor restrictions.

Additionally, the two net asset classes can be further disaggregated. For example, donor-restricted net assets can be broken down into (1) the amount maintained in perpetuity and (2) the amount expected to be spent over time or for a particular purpose.

Net assets without donor restrictions that are designated by the boardfor a specific use should be disclosed either on the face of the financial statements or in a footnote disclosure.

Sample Presentation of Net Assets

Here’s a sample presentation:

Net Assets

Without donor restrictions

Undesignated

$XX

Designated by Board for endowment

XX

XX

With donor restrictions

Perpetual in nature

XX

Purchase of equipment

XX

Time-restricted

XX

XX

Total Net Assets

$XX

Net Assets Released from “With Donor Restrictions”

The nonprofit should disaggregate the net assets released from restrictions:

program restrictions satisfaction

time restrictions satisfaction

satisfaction of equipment acquisition restrictions

appropriation of donor endowment and subsequent satisfaction of any related donor restrictions

satisfaction of board-imposed restriction to fund pension liability

Here’s an example from ASU 2016-14:

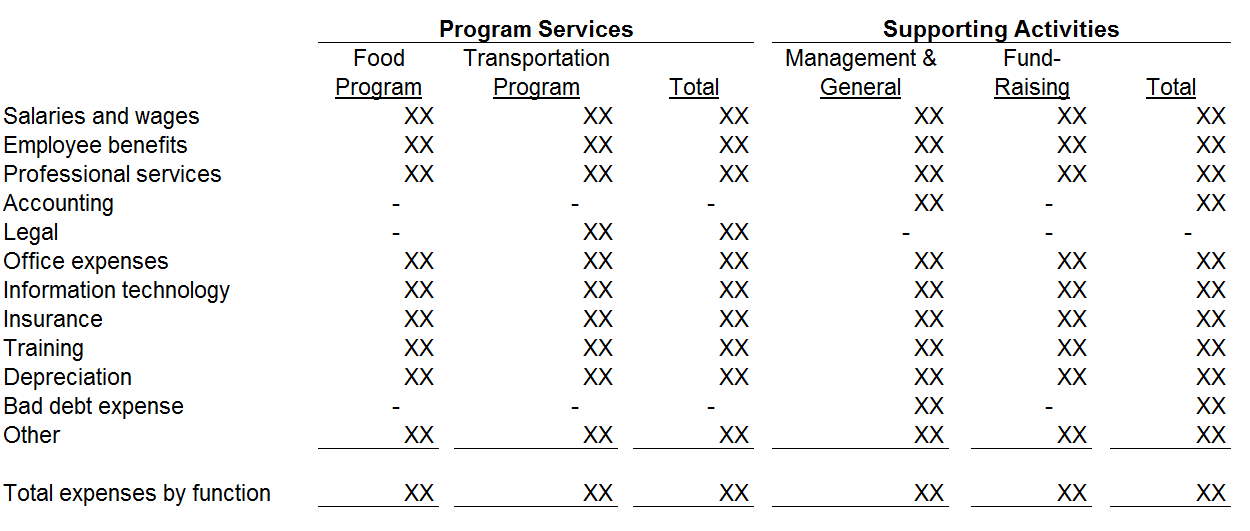

Presentation of Expenses

Presently, nonprofits must present expenses by function. So, nonprofits must present the following (either on the face of the statements or in the notes):

Program expenses

Supporting expenses

The new standard requires the presentation of expenses by function and nature (for all nonprofits). Nonprofits must also provide the analysis of these expenses in one location. Potential locations include:

Face of the statement of activities

A separate statement (preceding the notes; not as a supplementary schedule)

Notes to the financial statements

I plan to add a separate statement (like the format below) titled Statement of Functional Expenses. (Nonprofits should consider whether their accounting system can generate expenses by function and by nature. Making this determination now could save you plenty of headaches at the end of the year.)

External and direct internal investment expenses are netted with investment income and should not be included in the expense analysis. Disclosure of the netted expenses is no longer required.

Example of Expense Analysis

Here’s an example of the analysis, reflecting each natural expense classification as a separate row and each functional expense classification as a separate column.

The nonprofit should also disclose how costs are allocated to the functions. For example:

Certain expenses are attributable to more than one program or supporting function. Depreciation is allocated based on a square-footage basis. Salaries, benefits, professional services, office expenses, information technology and insurance, are allocated based on estimates of time and effort.

Intermediate Measure of Operations

If the nonprofit provides a measure of operations on the face of the financial statements and the use of the term “operations” is not apparent, disclose the nature of the reported measure of operations or the items excluded from operations. For example:

Measure of Operations

Learning Disability’s operating revenue in excess of operating expenses includes all operating revenues and expenses that are an integral part of its programs and supporting activities and the assets released from donor restrictions to support operating expenditures. The measure of operations excludes net investment return in excess of amounts made available for operations.

Alternatively, provide the measure of operations on the face of the financial statements by including lines such as operating revenues and operating expenses in the statement of activities. Then the excess of revenues over expenses could be presented as the measure of operations.

Liquidity and Availability of Resources

FASB is shining the light on the nonprofit’s liquidity. Does the nonprofit have sufficient cash to meet its upcoming responsibilities?

Nonprofits should include disclosures regarding the liquidity and availability of resources. The purpose of the disclosures is to communicate whether the organization’s liquid available resources are sufficient to meet the cash needs for general expenditures for one year beyond the balance sheet date. The disclosure should be qualitative (providing information about how the nonprofit manages its liquid resources) and quantitative (communicating the availability of resources to meet the cash needs).

Sample Liquidity and Availability Disclosure

The FASB Codification provides the following example disclosure in 958-210-55-7:

NFP A has $395,000 of financial assets available within 1 year of the balance sheet date to meet cash needs for general expenditure consisting of cash of $75,000, contributions receivable of $20,000, and short-term investments of $300,000. None of the financial assets are subject to donor or other contractual restrictions that make them unavailable for general expenditure within one year of the balance sheet date. The contributions receivable are subject to implied time restrictions but are expected to be collected within one year.

NFP A has a goal to maintain financial assets, which consist of cash and short-term investments, on hand to meet 60 days of normal operating expenses, which are, on average, approximately $275,000. NFP A has a policy to structure its financial assets to be available as its general expenditures, liabilities, and other obligations come due. In addition, as part of its liquidity management, NFP A invests cash in excess of daily requirements in various short-term investments, including certificate of deposits and short-term treasury instruments. As more fully described in Note XX, NFP A also has committed lines of credit in the amount of $20,000, which it could draw upon in the event of an unanticipated liquidity need.

Alternatively, the nonprofit could present tables (see 958-210-55-8) to communicate the resources available to meet cash needs for general expenditures within one year of the balance sheet date.

Cash Flow Statement Presentation

A nonprofit can use the direct or indirect method to present its cash flow information. The reconciliation of changes in net assets to cash provided by (used in) operating activities is not required if the direct method is used.

Consider whether you want to incorporate additional changes that will be required by ASU 2016-18, Statement of Cash Flows–Restricted Cash. If your nonprofit has no restricted cash, then this standard is not applicable.

You can early implement ASU 2016-18. (The effective date is for fiscal years beginning after December 15, 2018.) Once this standard is effective, you’ll include restricted cash in your definition of cash. The last line of the cash flow statement might read as follows: Cash, Cash Equivalents, and Restricted Cash.

Effective Date of ASU 2016-14

The effective date for 2016-14, Not-for-Profit Entities, is for fiscal periods beginning after December 15, 2017 (2018 calendar year-ends and 2019 fiscal year-ends). The standard can be early adopted.

For comparative statements, apply the standard retrospectively.

If presenting comparative financial statements, the standard does allow the nonprofit to omit the following information for any periods presented before the period of adoption:

Analysis of expenses by both natural classification and functional classification (the separate presentation of expenses by functional classification and expenses by natural classification is still required). Nonprofits that previously were required to present a statement of functional expenses do not have the option to omit this analysis; however, they may present the comparative period information in any of the formats permitted in ASU 2014-16, consistent with the presentation in the period of adoption.

Disclosures related to liquidity and availability of resources.

The variable interest entity (VIE) considerations just got much easier. FASB is—with ASU 2018-17—providing another get-out-of-jail-free card to private companies.

When FASB originally issued its VIE accounting guidance many years ago, it created a thorny issue for private companies—one almost incomprehensible to anyone but a seasoned CPA. FASB required companies to consider whether entities under common control should be consolidated, even if the reporting entity did not own a majority of the voting stock. While FASB’s intent was noble (it was addressing issues that arose from Enron’s use of special purpose entities), it created one of the most difficult accounting standards ever. In the ensuing years, private companies begged for relief. The first leg of that relief came with the issuance of ASU 2014-07 (more in a moment); the second leg of that relief comes now with ASU 2018-17.

The original VIE accounting guidance issued in the early 2000s required reporting entities to consolidate related companies if certain conditions were met. For example, if a reporting entity rented real estate from a commonly owned company, then consolidation might be required. This original guidance applied to both public and private companies. Public companies tend to have the muscle and knowledge to make these complicated evaluations. Not so for private companies. That’s why private companies asked for relief.

First, FASB had issued ASU 2014-07, Consolidation (Topic 810): Applying Variable Interest Entities Guidance to Common Control Leasing Arrangements. That standard allowed reporting entities, when specified conditions were met, to not consolidate lessee companies. A private company could elect to not apply variable interest entity guidance to a lessor entity if those specified conditions were met.

Then, on October 31, 2018, FASB issued Accounting Standards Update (ASU) 2018-17, Consolidation (Topic 810):Targeted Improvements to Related Party Guidance for Variable Interest Entities. ASU 2018-17 expands the provisions in ASU 2014-07, permitting the accounting alternative to include all private company common control arrangements(see criteria below).

VIE Accounting Alternative

Using 2018-17, a legal entity need not be evaluated by a private company (reporting entity) under the VIE accounting model if all of the following are true:

The reporting entity and the legal entity are under common control.

The reporting entity and the legal entity are not under common control of a public business entity.

The legal entity under common control is not a public business entity.

The reporting entity does not directly or indirectly have a controlling financial interest in the legal entity when considering the voting interest model (see ASC 810-10-05; under the voting interest model, the usual condition for a controlling financial interest is ownership by one reporting entity, directly or indirectly, of more than 50 percent of the outstanding voting shares of another entity).

The Alternative is an Election

Applying this accounting alternative is an accounting policy election. If the election is made, then the private company must apply the criteria above to all legal entities. If, for example, a reporting entity has consolidated companies A and B due to VIE considerations, the election must be applied to both entities.

Combined Financial Statements (Still an Option)

If a private company reporting entity makes the alternative election, it can still create combined financial statements for entities under common control. For example, if a reporting entity consolidates companies A and B under the prior VIE guidance, it might no longer do so after the election. Nevertheless, the reporting entity couldissue combined financial statements. The reporting entity might, for example, issue combined financial statements for the reporting entity and company B (and exclude company A). See ASC 810-10-55-1B.

Entities that Can’t Use the Alternative

The entities that can’t use the VIE alternative (under ASU 2018-17) include:

Public business entities

Not-for-profit entities

Employee benefit plans (within the scope of ASC 960, 962, and 965)

Required Disclosures

A private company that makes the election to use the alternative isrequired to include information about the relationship of the entities. Those disclosures include (see 810-10-50-2AG, 810-10-50-2AH and 810-10-50-2AI for complete list of disclosures):

The nature and risksas a result of the reporting entity’s involvement with the legal entity under common control

How a reporting entity’s involvement with the legal entity under common control affects:

Financial position

Financial performance

Cash flows

The carrying amounts and classification of the assets and liabilities in the reporting entity’s statement of financial positionas a result of its involvement with the legal entity under common control

The reporting entity’s maximum exposure to loss based on its relationship with the legal entity under common control (if not quantifiable, then that fact should be disclosed)

If the maximum exposure to loss exceeds the carrying amount of the assets and liabilities, that information is to be disclosed (including the terms of the arrangements)

Effective Dates

For entities other than private companies, the amendments in ASU 2018-17 are effective for fiscal years beginning after December 15, 2019, and interim periods within those fiscal years. The amendments in this Update are effective for a private company for fiscal years beginning after December 15, 2020, and interim periods within fiscal years beginning after December 15, 2021. All entities are required to apply the amendments in this Update retrospectively with a cumulative-effect adjustment to retained earnings at the beginning of the earliest period presented.

Are you preparing financial statements and wondering whether you need to include going concern disclosures? Or maybe you’re the auditor, and you’re wondering if a going concern paragraph should be added to the audit opinion. You’ve heard there are new requirements for both management and auditors, but you’re not sure what they are.

This article summarizes (in one place) the new going concern accounting and auditing standards.

Going Concern Standards

For many years the going concern standards were housed in the audit standards–thus, the need for FASB to issue accounting guidance (ASU 2014-15). It makes sense that FASB created going concern disclosure guidance. After all, disclosures are an accounting issue.

Going Concern Accounting Standard

ASU 2014-15, Disclosure of Uncertainties about an Entity’s Ability to Continue as a Going Concern, provides guidance in preparing financial statements. This standard was effective for years ending after December 15, 2016.

GASB Statement 56, Codification of Accounting and Financial Reporting Guidance Contained in the AICPA Statements on Auditing Standards, is the relevant going concern standard for governments. GASB 56 was issued in March 2009. (GASB 56 requires financial statement preparers to evaluate whether there is substantial doubt about a governmental entity’s ability to continue as a going concern for 12 months beyond the date of the financial statements. As you will see below, this timeframe is different from the one called for under ASU 2014-15. This post focuses on ASU 2014-15 and SAS 132.)

Meanwhile, the Auditing Standards Board issued their own going concern standard in February 2017: SAS 132.

Going Concern Auditing Standard

Auditors will use SAS 132, The Auditor’s Consideration of an Entity’s Ability to Continue as a Going Concern, to make going concern decisions. This SAS is effective for audits of financial statements for periods ending on or after December 15, 2017. SAS 132 amends SAS 126, The Auditor’s Consideration of an Entity’s Ability to Continue as a Going Concern.

So, let’s take a look at how to apply ASU 2014-15 and SAS 132.

Two Going Concern Decisions

In the past, the going concern decisions were made by auditors in a single step. Now, it is helpful to think of going concern decisions in two steps:

Management decisions concerning the preparation of financial statements

Auditor decisions concerning the audit of the financial statements

First, we’ll consider management’s decisions.

1. Management Decisions about Going Concern Accounting

ASU 2014-15 provides guidance concerning management’s determination of whether there is substantial doubt regarding the entity’s ability to continue as a going concern.

What is the Going Concern Accounting Definition?

FASB defines going concern with the words substantial doubt. So, how does FASB define substantial doubt?

Substantial doubt about the entity’s ability to continue as a going concern is considered to exist when aggregate conditions and events indicate that it is probable that the entity will be unable to meet obligations when due within one year of the date that the financial statements are issued or are available to be issued.

What is Probable?

So, how does management determine if “it is probable that the entity will be unable to meet obligations when due within one year”?

Probable means likely to occur.

If for example, a company expects to miss a debt service payment in the coming year, then substantial doubt exists. This initial assessment is made without regard to management’s plans to alleviate going concern conditions.

ASC 205-40-50-4 says:

The evaluation initially shall not take into consideration the potential mitigating effect of management’s plans that have not been fully implemented as of the date that the financial statements are issued (for example, plans to raise capital, borrow money, restructure debt, or dispose of an asset that have been approved but that have not been fully implemented as of the date that the financial statements are issued).

But what factors should management consider?

Factors to Consider

Management should consider the following factors when assessing going concern:

The reporting entity’s current financial condition, including the availability of liquid funds and access to credit

Obligations of the reporting entity due or new obligations anticipated within one year (regardless of whether they have been recognized in the financial statements)

The funds necessary to maintain operations considering the reporting entity’s current financial condition, obligations, and other expected cash flows

Other conditions or events that may affect the entity’s ability to meet its obligations

Moreover, management is to consider these factors for one year. But from what date?

Timeframe

The financial statement preparer (i.e., management or a party contracted by management) should assess going concern in light of one year from the date “the financial statements are issued or are available to be issued.”

So, if December 31, 2017, financial statements (for a nonpublic company) are available to be issued on March 15, 2017, the preparer looks forward one year from March 15, 2017. Then, the preparer asks, “Is it probable that the company will be unable to meet its obligations through March 15, 2018?” If yes, substantial doubt is present and disclosures are necessary. If no, then substantial doubt does not exist. As you would expect, the answer to this question determines whether going concern disclosures are to be made and what should be included.

Substantial Doubt Answer Determines Disclosures

If substantial doubt does not exist, then going concern disclosures are not necessary.

If substantial doubt exists, then the company needs to decide if management’s plans alleviate the going concern issue. This decision determines the disclosures to be made. The required disclosures are based upon whether:

Management’s plans alleviate the going concern issue

Management’s plans do not alleviate the going concern issue

What if Management’s Plans Alleviate the Going Concern Issue?

If conditions or events raise substantial doubt about an entity’s ability to continue as a going concern, but the substantial doubt is alleviated as a result of consideration of management’s plans, the entity should disclose information that enables users of the financial statements to understand all of the following (or refer to similar information disclosed elsewhere in the footnotes):

Principal conditions or events that raised substantial doubt about the entity’s ability to continue as a going concern (before consideration of management’s plans)

Management’s evaluation of the significance of those conditions or events in relation to the entity’s ability to meet its obligations

Management’s plans that alleviated substantial doubt about the entity’s ability to continue as a going concern

Management’s plans should be considered only if is it probable that they will be effectively implemented. Also, it must be probable that management’s plans will be effective in alleviating substantial doubt.

So, if management’s plans are expected to work, does the company have to explicitly state that management’s plans will alleviate substantial doubt? No.

When management’s plans alleviate substantial doubt, companies need not use the words going concern or substantial doubt in the disclosures. And as Sears discovered, it may not be wise to do so (their shares dropped 16% after using the term substantial doubt even though management had plans to alleviate the risk). Rather than using the term substantial doubt, consider describing conditions (e.g., cash flows are not sufficient to meet obligations) and management plans to alleviate substantial doubt.

The Company had losses of $4,525,123 in the year ending March 31, 2017. As of March 31, 2017, its accumulated deficit is $11,325,354.

Management believes the Company’s present cash flows will not enable it to meet its obligations for twelve months from the date these financial statements are available to be issued. However, management is working to obtain new long-term financing. It is probable that management will obtain new sources of financingthat will enable the Company to meet its obligations for the twelve-month period from the date the financial statements are available to be issued.

Notice this example does not use the words substantial doubt.

What if Management’s Plans Do Not Alleviate the Going Concern Issue?

If conditions or events raise substantial doubt about an entity’s ability to continue as a going concern, and substantial doubt is not alleviated after consideration of management’s plans, an entity should include a statement in the notes indicating that there is substantial doubt about the entity’s ability to continue as a going concern within one year after the date that the financial statements are available to be issued (or issued when applicable). Additionally, the entity should disclose information that enables users of the financial statements to understand all of the following:

Principal conditions or events that raise substantial doubt about the entity’s ability to continue as a going concern

Management’s evaluation of the significance of those conditions or events in relation to the entity’s ability to meet its obligations

Management’s plans that are intended to mitigate the conditions or events that raise substantial doubt about the entity’s ability to continue as a going concern

Sample Going Concern Disclosure – Substantial Doubt Not Alleviated

An example disclosure follows:

Note 2 – Going Concern

The financial statements have been prepared on a going concern basis which assumes the Company will be able to realize its assets and discharge its liabilities in the normal course of business for the foreseeable future. The Company had losses of $1,232,555 in the current year. The Company has incurred accumulated losses of $2,891,727 as of March 31, 2017. Cash flows used in operations totaled $555,897 for the year ended March 31, 2017.

Management believes these conditions raise substantial doubt about the Company’s ability to continue as a going concern within the next twelve months from the date these financial statements are available to be issued. The ability to continue as a going concern is dependent upon profitable future operations, positive cash flows, and additional financing.

Management intends to finance operating costs over the next twelve months with existing cash on hand and loans from its directors. Management is also working to secure new bank financing. The Company’s ability to obtain the new financing is not known at this time.

Notice this note includes a statement that substantial doubt is present. Though management’s plans are disclosed, the probability of success is not provided.

Going Concern Accounting Summary

ASU 2014-15 focuses on management’s assessment regarding whether substantial doubt exists. If substantial doubt exists, then disclosures are required. Here’s a short video summarizing 2014-15:

Thus far, we’ve addressed the stage 1. management decisions. As you can see management’s considerations focus on disclosures. By contrast, auditors focus on the audit opinion. Now, let’s look at what auditors must do.

2. Auditor Decisions Regarding Going Concern

SAS 132 provides guidance concerning the auditor’s consideration of an entity’s ability to continue as a going concern.

Auditing Going Concern Accounting

SAS 132, paragraph 10, states the objectives of the auditor are as follows:

Obtain sufficient appropriate audit evidenceregarding, and to conclude on, the appropriateness of management’s use of the going concern basis of accounting, when relevant, in the preparation of the financial statements

Conclude, based on the audit evidence obtained, whether substantial doubt about an entity’s ability to continue as a going concern for a reasonable period of time exists

Evaluate the possible financial statement effects, including the adequacy of disclosure regarding the entity’s ability to continue as a going concern for a reasonable period of time

Report in accordance with this SAS

These objectives can be summarized as follows:

Conclude about whether the going concern basis of accounting is appropriate

Determine whether substantial doubt is present

Determine whether the going concern disclosures are adequate

Issue an appropriate opinion

In light of these objectives, certain audit procedures are necessary.

Risk Assessment Procedures

In the risk assessment phase of an audit, the auditor should consider whether conditions or events raise substantial doubt. In doing so, the auditor should examine any preliminary management evaluation of going concern. If such an evaluation was performed, the auditor should review it with management. If no evaluation has occurred, then the auditor should discuss with management the appropriateness of using the going concern basis of accounting (the liquidation basis of accounting is required by ASC 205-30 when the entity’s liquidation is imminent) and whether there are conditions or events that raise substantial doubt.

The auditor is to consider conditions and events that raise substantial doubt about an entity’s ability to continue as a going concern for areasonable period of time. What is a reasonable period of time? It is the period of time required by the applicable financial reporting framework or, if no such requirement exists, within one year after the date that the financial statements are issued (or within one year after the date that the financial statements are available to be issued, when applicable). The governmental accounting standards require an evaluation period of “12 months beyond the date of the financial statements.”

Auditors should consider negative financial trends or factors such as:

Working capital deficiencies

Negative cash flows from operating activities

Default on loans

A denial of trade credit from suppliers

Need to restructure debt

Need to dispose of assets

Work stoppages or other labor problems

Need to significantly revise operations

Legal problems

Loss of key customers or suppliers

Uninsured catastrophes

The need for new capital

The risk assessment procedures are a part of planning an audit. You may obtain new information as you perform the engagement.

Remaining Alert Throughout the Audit

The auditor should remain alert throughout the audit for conditions or events that raise substantial doubt. So, after the initial review of going concern issues in the planning stage, the auditor considers the impact of new information gained during the subsequent stages of the engagement.

Audit Procedures When Substantial Doubt is Present

If events or conditions do give rise to substantial doubt, then the audit procedures should include the following (SAS 132, paragraph 16.):

Requesting management to make an evaluation when management has not yet performed an evaluation

Evaluating management’s plans in relation to its going concern evaluation, with regard to whether it is probable that:

management’s plans can be effectively implemented and

the plans would mitigate the relevant conditions or events that raise substantial doubt about the entity’s ability to continue as a going concern for a reasonable period of time

When the entity has prepared a cash flow forecast, and analysis of the forecast is a significant factor in evaluating management’s plans:

evaluating the reliability of the underlying data generated to prepare the forecast and

determining whether there is adequate support for the assumptions underlying the forecast, which includes considering contradictory audit evidence

Considering whether any additional facts or information have become available since the date on which management made its evaluation

Sometimes management’s plans to alleviate substantial doubt include financial support by third parties or owner-managers (usually referred to as supporting parties).

Financial Support by Supporting Parties

When financial support is necessary to mitigate substantial doubt, the auditor should obtain audit evidence about the following:

The intent of such supporting parties to provide the necessary financial support, including written evidence of such intent, and

The ability of such supporting parties to provide the necessary financial support

If the evidence in a. is not obtained, then “management’s plans are insufficient to alleviate the determination that substantial doubt exists.”

Intent of Supporting Parties

The intent of supporting parties may be evidenced by either of the following:

Obtaining from management written evidence of a commitment from the supporting party to provide or maintain the necessary financial support (sometimes called a “support letter”)

Confirming directly with the supporting parties (confirmation may be needed if management only has oral evidence of such financial support)

If the auditor receives a support letter, he can still request a written confirmation from the supporting parties. For instance, the auditor may desire to check the validity of the support letter.

If the support comes from an owner-manager, then the written evidence can be a support letter or a written representation.

Support Letter

An example of a third party support letter (when the applicable reporting framework is FASB ASC) is as follows:

(Supporting party name) will, and has the ability to, fully support the operating, investing, and financing activities of (entity name) through at least one year and a day beyond [insert date] (the date the financial statements are issued or available for issuance, when applicable).

You can specify a date in the support letter that is later than the expected date. That way if there is a delay, you may be able to avoid updating the letter.

The auditor should not only consider the intent of the supporting parties but the ability as well.

Ability of Supporting Parties

The ability of supporting parties to provide support can be evidenced by information such as:

Proof of past funding by the supporting party

Audited financial statements of the supporting party

Bank statements and valuations of assets held by a supporting party

After examining the intent and ability of supporting parties regarding the one-year period, you might identify potential going concern problems that will occur more than one year out.

Conditions and Events After the Reasonable Period of Time

So, should an auditor inquire about conditions and events that may affect the entity’s ability to continue as a going concern beyond management’s period of evaluation (i.e., one year from the date the financial statements are available to be issued or issued, as applicable)? Yes.

Suppose an entity knows it will be unable to meet its November 15, 2018, debt balloon payment. The financial statements are available to be issued on June 15, 2017, so the reasonable period goes through June 15, 2018. But management knows it can’t make the balloon payment, and the bank has already advised that the loan will not be renewed. SAS 132 requires the auditor to inquire of management concerning their knowledge of such conditions or events.

Why? Only to determine if any potential (additional) disclosures are needed. FASB only requires the evaluation for the year following the date the financial statements are issued (or available to be issued, as applicable). Events following this one year period have no bearing on the current year going concern decisions. Nevertheless, additional disclosures may be merited.

Thus far, the requirements to evaluate the use of the going concern basis of accounting and whether substantial doubt is present have been explained. Now, let’s see what the requirements are for:

Written representations from management

Communications with those charged with governance

Documentation

Written Representations When Substantial Doubt Exists

When substantial doubt exists, the auditor should request the following written representations from management:

A description of management’s plans that are intended to mitigate substantial doubt and the probability that those plans can be effectively implemented

That the financial statements disclose all the matters relevant to the entity’s ability to continue as a going concern including conditions and events and management’s plans

Communications with Those Charged with Governance

Remember that you may need to add additional language to your communication with those charged with governance.

When conditions and events raise substantial doubt about the entity’s ability to continue as a going concern for a reasonable period of time, the auditor should communicate the following (unless those charged with governance manage the entity):

Whether the conditions or events, considered in the aggregate, that raise substantial doubt about an entity’s ability to continue as a going concern for a reasonable period of time constitute substantial doubt

The auditor’s consideration of management’s plans

Whether management’s use of the going concern basis of accounting, when relevant, is appropriate in the preparation of the financial statements

The adequacy of related disclosures in the financial statements

The implications for the auditor’s report

Documentation Requirements

When substantial doubt exists before consideration of management’s plans, the auditor should document the following (SAS 132, paragraph 32.):

The conditions or events that led the auditor to believe that there is substantial doubt about the entity’s ability to continue as a going concern for a reasonable period of time.

The elements of management’s plans that the auditor considered to be particularly significant to overcomingthe conditions or events, considered in the aggregate, that raise substantial doubt about the entity’s ability to continue as a going concern, if applicable.

The audit procedures performed to evaluate the significant elements of management’s plans and evidence obtained, if applicable.

The auditor’s conclusion regarding whether substantial doubt about the entity’s ability to continue as a going concern for a reasonable period of time remains or is alleviated. If substantial doubt remains, the auditor should also document the possible effects of the conditions or events on the financial statements and the adequacy of the related disclosures. If substantial doubt is alleviated, the auditor should also document the auditor’s conclusion regarding the need for, and, if applicable, the adequacy of, disclosure of the principal conditions or events that initially caused the auditor to believe there was substantial doubt and management’s plans that alleviated the substantial doubt.

The auditor’s conclusion with respect to the effects on the auditor’s report.

Opinion – Emphasis of Matter Regarding Going Concern

If the auditor concludes that there is substantial doubt concerning the company’s ability to continue as a going concern, an emphasis of a matter paragraph should be added to the opinion.

An example of a going concern paragraph is as follows:

The accompanying financial statements have been prepared assuming that the Company will continue as a going concern. As discussed in Note 2 to the financial statements, the Company has suffered recurring losses from operations, has a net capital deficiency, and has stated that substantial doubt exists about the company’s ability to continue as a going concern. Management’s evaluation of the events and conditions and management’s plans regarding these matters are also described in Note 2. The financial statements do not include any adjustments that might result from the outcome of this uncertainty. Our opinion is not modified with respect to this matter.

The auditor should not use conditional language regarding the existence of substantial doubt about the entity’s ability to continue as a going concern.

Opinion – Inadequate Going Concern Disclosures

Paragraph 26. of SAS 132 states that an auditor should issue a qualified opinion or an adverse opinion, as appropriate, when going concern disclosures are not adequate.

Going Concern Auditing Summary

Now, let’s circle back to where we started and review the objectives of SAS 132.

The objectives are as follows:

Conclude about whether the going concern basis of accounting is appropriate

Determine whether substantial doubt is present

Determine whether the going concern disclosures are adequate

Issue an appropriate opinion

Conclusion

As you can see ASU 2014-15 and SAS 132 are complex. So, make sure you are using the most recent updates to your disclosure checklists and audit forms and programs.

ASU 2015-11 requires that entities measure inventory at the lower of cost or net realizable value (LCNRV), provided they don’t use the last-in-first-out method (LIFO) or the retail inventory method. Entities using LIFO or the retail inventory method will continue to use the lower of cost or market (where market is replacement cost). Entities using the first-in-first-out (FIFO), average cost, or any other cost flow methods (other than LIFO and the retail inventory methods) should use the lower of cost or net realizable value approach.

So, where applicable, market is being replaced by net realizable value.

The Financial Accounting Standards Board’s glossary defines net realizable value as follows:

Estimated selling prices in the ordinary course of business, less reasonably predictable costs of completion, disposal, and transportation.

Why the change? FASB is working to simplify some accounting standards. FASB had received comments from stakeholders that the requirement to subsequently measure inventory was “unnecessarily complex because there are several potential outcomes.”

Why did FASB not require the LCNRV method for all entities? The summary section of ASU 2015-11 says, “The Board received feedback from stakeholders that the proposed amendments would reduce costs and increase comparability for inventory measured using FIFO or average cost but potentially could result in significant transition costs that would not be justified by the benefits for inventory measured using LIFO or the retail inventory method…Therefore, the Board decided to limit the scope of the simplification to exclude inventory measured using LIFO or the retail inventory method.”

What Disclosure is Required for the Change in Accounting Principle?

BC16 of ASU 2015-11 states the following:

The Board decided that the only disclosures required at transition should be the nature of and reason for the change in accounting principle. The Board concluded that the costs of a quantitative disclosure about the change from the lower of cost or market to the lower of cost and net realizable value would not justify the benefits because a reporting entity would be required in the year of adoption to measure inventory using both existing requirements and the amendments in this Update, and because the change would not be significant for some entities.

An entity is required only to disclose the nature and reason for the change in accounting principle in the first interim and annual period of adoption.

Sample ASU 2015-11 Disclosures

Here is a sample disclosure from Mercer International Inc.’s 10-K:

Accounting Pronouncements Implemented

In July 2015, the FASB issued Accounting Standards Update 2015-11, Simplifying the Measurement of Inventory (“ASU2015–11”) which requires that inventory within the scope of this update, including inventory stated at average cost, be measured at the lower of cost and net realizable value. This update is effective for financial statements issued for fiscal years beginning after December 15, 2016. The adoption of ASU2015–11 did not impact the Company’s financial position.

Here is a sample disclosure from Delta Apparel, Inc.’s 10-K:

Recently Issued Accounting Pronouncements Not Yet Adopted

In July 2015, the FASB issued ASU No. 2015-11, Simplifying the Measurement of Inventory, (“ASU2015–11“). This new guidance requires an entity to measure inventory at the lower of cost and net realizable value. Currently, entities measure inventory at the lower of cost or market. ASU2015–11 replaces market with net realizable value. Net realizable value is the estimated selling price in the ordinary course of business, less reasonably predictable costs of completion, disposal, and transportation. Subsequent measurement is unchanged for inventory measured under last-in, first-out or the retail inventory method. ASU2015–11 requires prospective adoption for inventory measurements for fiscal years beginning after December 15, 2016, and interim periods within those years for public business entities. Early application is permitted. ASU2015–11 will, therefore, be effective in our fiscal year beginning October 1, 2017. We are evaluating the effect that ASU2015–11 will have on our Consolidated Financial Statements and related disclosures, but do not believe it will have a material impact.

Here is a sample disclosure from Dr. Pepper Snapple Group, Inc.’s 10-K:

Recently Adopted Provisions of U.S. GAAP

As of January 1, 2017, the Company adopted ASU2015–11, Inventory (Topic 330): Simplifying the Measurement of Inventory (“ASU2015–11“). ASU2015–11 requires inventories measured under any methods other than last-in, first-out (“LIFO”) or the retail inventory method to be subsequently measured at the lower of cost or net realizable value, rather than at the lower of cost or market. Subsequent measurement of inventory using LIFO or the retail inventory method is unchanged by ASU2015–11. The adoption of ASU2015–11 did not have a material impact on the Company’s consolidated financial statements.

Effective Dates for ASU 2015-11

For public business entities, the amendments are effective for fiscal years beginning after December 15, 2016, including interim periods within those fiscal years. For all other entities, the amendments are effective for fiscal years beginning after December 15, 2016, and interim periods within fiscal years beginning after December 15, 2017. The amendments should be applied prospectively with earlier application permitted as of the beginning of an interim or annual reporting period.