Charles Hall is a practicing CPA and Certified Fraud Examiner. For the last thirty-five years, he has primarily audited governments, nonprofits, and small businesses.

He is the author of The Little Book of Local Government Fraud Prevention, The Why and How of Auditing, Audit Risk Assessment Made Easy, and Preparation of Financial Statements & Compilation Engagements. He frequently speaks at continuing education events.

Charles consults with other CPA firms, assisting them with auditing and accounting issues.

Do you ever need to solve accounting problems quickly?

I often hear the words, “Hey Charles, I’ve got a quick question,” and they launch into their issue, hopeful I can look into my crystal ball and give them an answer. As it turns out, I do have one. I keep it on my desktop. You probably have one too.

Most CPAs, when confronted with an accounting Gordian Knot, begin their quest to cut through the problem with their mighty sword–the GAAP Guide. Ah, an excellent choice for sure, but is it the best place to start? Or how about the granddaddy of them all? The FASB Codification. Another fine choice, but it’s an 800-pound gorilla. So where’s the best place to start? Thecrystal ball.

And what is the crystal ball? It’s your disclosure checklist.

You say, “but it’s just a laundry list of accounting requirements.” Yes, but it’s a great pointer (to answers).

To solve accounting problems quickly, do a word search in your disclosure checklist. My checklist is in Word, so I use the find feature (click control, find) to locate a keyword. Try to use a unique word where possible–such as noninterest or contingent. You may have to click next a few times to locate the relevant text. Once you find the relevant text, the pathway to your solution lies before you: the checklist provides you with the applicable FASB Codification ASC section (e.g., 850-10-50-5).You can key the number in the FASB Codification or your research libraryto find your answer.

Now you can provide a quick answer to that difficult question (and look like a genius). When your peers ask, “How did you find the answer so quickly?” Tell them, “My crystal ball.”

The auditor should use external confirmation procedures for accounts receivable, except when one or more of the following is applicable:

The overall account balance is immaterial.

External confirmation procedures for accounts receivable would be ineffective.

The auditor’s assessed level of risk of material misstatement at the relevant assertion level is low, and the other planned substantive procedures address the assessed risk. In many situations, the use of external confirmation procedures for accounts receivable and the performance of other substantive procedures are necessary to reduce the assessed risk of material misstatement to an acceptably low level.

If receivables are material and confirmation procedures will be effective, then confirmations must be sent. (Normally, the existence assertion related to receivables is moderate to high. So, 3. above is not in play.)

When are Confirmations Ineffective?

AU-C 330.A56 states:

External confirmation procedures may be ineffective when based on prior years’ audit experience or experience with similar entities:

response rates to properly designed confirmation requests will be inadequate; or

responses are known or expected to be unreliable.

If the auditor has experienced poor response rates to properly designed confirmation requests in prior audits, the auditor may instead consider changing the manner in which the confirmation process is performed, with the objective of increasing the response rates or may consider obtaining audit evidence from other sources.

Alternative Procedures When Confirmations are not Sent

What audit procedure should be performed if confirmations are not sent? Usually, the auditor will examine cash collections after the period-end. Care must be taken to ensure that the subsequent collections examined relate to receivables that existed at period-end and not to sales occurring after period-end.

Required Documentation When Confirmations are not Sent

AU-C 330.31 states that “the auditor should include in the audit documentation the basis for any determination not to use external confirmation procedures for accounts receivable when the account balance is material.” So, it is not sufficient to simply state that the use of confirmations is ineffective. We should state that we tried to confirm receivables in a prior year without effective results or that we tried to confirm receivables for clients in a similar industry, but without effective results.

The auditor should include a memo to the file or add comments on the receivables work paper explaining why confirmations were not sent.

A: While not required, it is advisable to provide management letters when performing SSARS services. Why? Two reasons: (1) It’s a way to add value to the engagement, and (2) it’s a way to protect yourself from potential litigation. Clients do–sometimes–sue CPAs in these so-called “lower risk” engagements. If we see control weaknesses (while performing a compilation for example), we should communicate those–even though standards don’t require it. Then, if theft occurs in that area and you are later sued regarding the fraud, you have a defense. If you don’t issue a management letter, at least send an email regarding the issues noted and retain a copy.

Q: Why obtain an engagement letter for nonattest services such as bookkeeping and tax (standards don’t require it)?

A: In all engagements, we want to state exactly what we are doing. Why? So, it is obvious what the client has hired us to do–and what they have not hired us to do. If a client says, “I told you to do my monthly bookkeeping and to file my property tax returns,” but you have no recollection of being asked to perform the latter, you need an engagement letter that specifies monthly bookkeeping (and nothing else).

Q: Should I say–in a bookkeeping engagement letter–the service is not designed to prevent fraud?

A: We should obtain a signed engagement letter for bookkeeping services, even though not required by standards. And yes, by all means, include a statement that the bookkeeping service is not designed to detect or prevent fraud.

Q: If I note fraud while performing a bookkeeping, preparation, compilation, or review engagement, should I report it to the appropriate levels of management?

A: Standards require this communication for review engagements. I would do likewise for the other services.

Q: Am I required to be independent if I perform bookkeeping and preparation services?

A: No, since both are nonattest services.

Q: If I create financial statements as a byproduct of an 1120 tax return, am I subject to AR-C 70 Preparation of Financial Statements?

A: No, you are only subject to AR-C 70 if you are engaged to prepare financial statements.

Q: If I perform bookkeeping services in a cloud-based accounting package such as QuickBooks, am I subject to AR-C 70?

A: It depends. Yes, if you are engaged to prepare financial statements. No, if you were not engaged to prepare financial statements. Who “pushes the button” to print the financial statements has no bearing on the applicability of AR-C 70.

Q: Am I required to have a signed engagement letter for all preparation, compilation and review engagements?

A: Yes.

Q: Can I act as a controller-for-hire and perform a compilation engagement?

A: Yes, but you need to state that you are not independent in the compilation report.

Q: Can I act as the controller-for-hire and perform a review engagement?

A: No. Independence is required for review engagements.

Q: If I prepare financial statements and perform a compilation, am I performing one service or are these considered two separate services?

A: They are two separate services. The preparation is a nonattest service, and the compilation is an attest engagement. Both can be specified in one engagement letter.

Here’s a video explaining the differences in preparation and compilation services.

Do you ever find yourself digging through hundreds of emails to find one message? You know it’s there somewhere, but you can’t put your electronic finger on it. Use Slack to communicate by project–that way, you’ll have all messages (by project, e.g., individual audit engagement) in one place.

What is Slack?

Slack is software designed to allow project teams–e.g., audit team–to send and store messages. Why use Slack rather than traditional email? Messages are stored by channel (by project), making itmuch easier to see project conversations.

The Slack website says the following:

Most conversations in Slack are organized into public channels which anyone on your team can join. You can also send messages privately, but the true power of Slack comes from having conversations everyone on the team can see. This transparency means it’s quick to find out what’s going on all across the team, and when someone new joins, all the information they need is laid out, ready for them to read up on.

How CPAs Use Slack

How can you as a CPA or auditor use Slack?

Create a channel for each project, and ask all team members to communicate using Slack (rather than email).

In CPA firms, some activities are year-round such as quality control reviews (we perform several hundred a year). Other activities are a true project, such as an audit engagement. Either way, you can use a separate (Slack) channel to communicate and store all related messages.

Using Slack for Quality Control Reviews — An Example

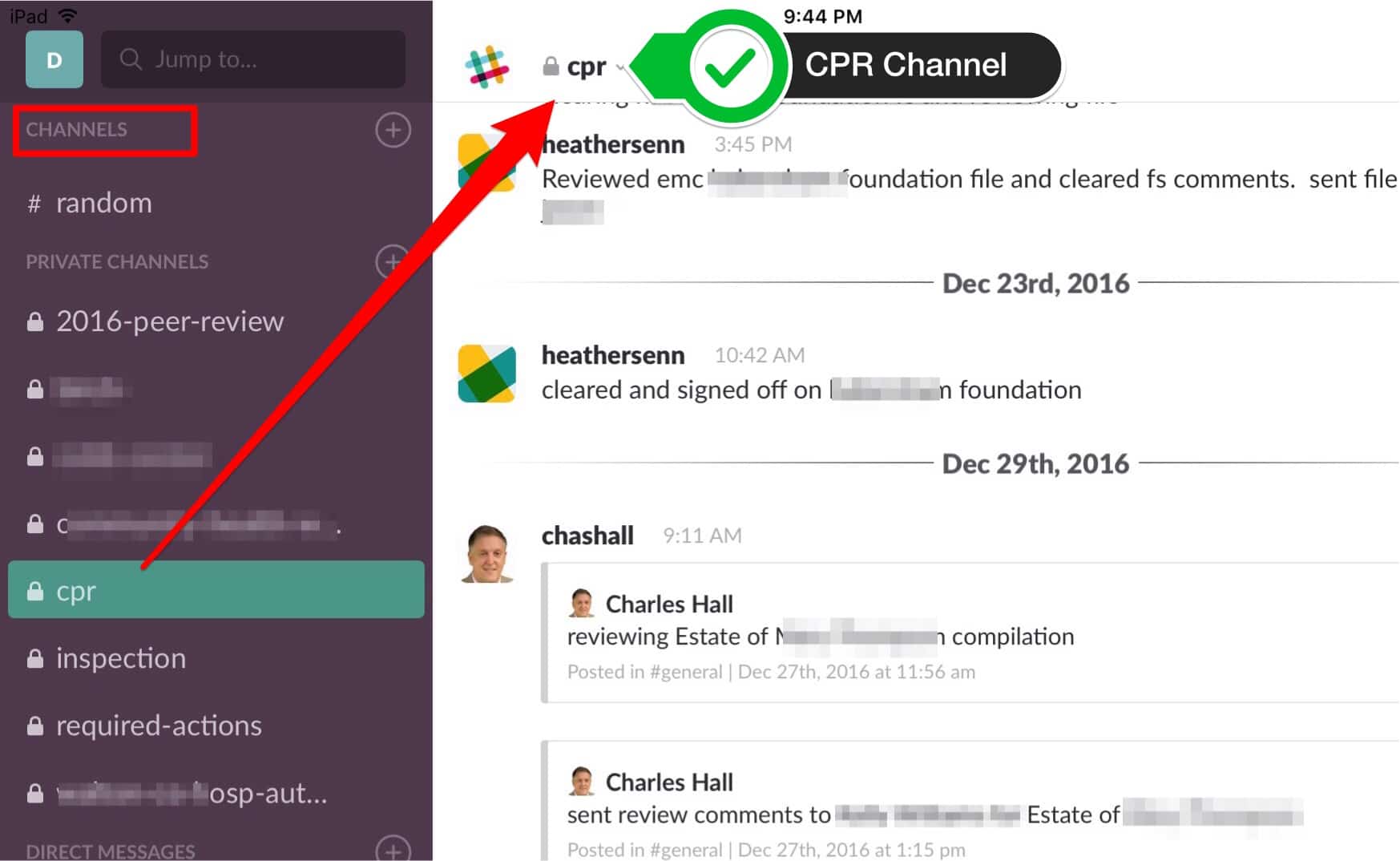

Below you see an example of how Heather, my associate, and I use Slack to communicate about file reviews in our quality control department. By doing so, we can see who is doing what and when. Also, all of the messages are searchable by channel. So, suppose I’m wondering when we reviewed the ABC Bank engagement. I can search the CPR (cold partner review) channel to see who performed the review and when. Notice, in this channel, Heather and Iare posting status comments. We do so for the following reasons:

To create a history of each review

To notify each other that the review has commenced (Slack automatically sends a notification message to those included in a channel)

To select our quality control channel, I click the CPR channel on the left (where all the channels appear). Once I click CPR, I see the most recent messages for this channel.

Made with Stitcher

Audits – Another Example

Think about a typical audit. You have three to five team members, with some individuals coming and going. To maintain continuity, you need a message board that allows all audit team members to see what is going on. That’s what Slack does when you create a channel for a particular audit. Think of it as a message board in the cloud since the designated personnel can see the audit communications with their PC, iPad, or cell phone.

Other Advantages of Slack

Advantages of Slack include the following:

Accessibility from all devices, including cell phones and tablets

Shareability of documents such as PDFs and spreadsheets

Configurable notifications of messages to team members

Private messaging (when needed)

Basic plan is free

Give It a Try

The best way to see how Slack works is to try it yourself. You don’t need any training since it’s easy to use. To see more information about Slack, click here.